This is really well developed and I support the protocol changes described in RPIP-49. Looking forward to the vote. This is a great step forward for Rocket Pool’s DAO governance too.

6 Likes

that looks good to me

Hello. I have some questions on the proposed NO rewards and RPL value capture mechanisms:

Iiuc, post tokenomics rework:

- Total protocol revenue = 14% of borrowed staking returns in ETH

- Protocol revenue split, all paid in ETH:

a) 5% (35.71% total revenue) to ETH-only NOs

b) 5% (35.71%) to NOs with staked RPL (proportional to share of staked RPL)

c) 4% (28.57%) to either RPL value accrual OR to NOs with staked RPL, same as above

Questions:

- Why separate ETH-only NOs from NOs with staked RPL? Seems unnecessary and could lead to some unanticipated behaviour. See next point.

- Why do RPL hodlers need to be a NO to stake RPL? What about non-NOs staking RPL and earning ETH, similar to GMX staking? So NOs are just NOs and anyone including NOs can stake RPL.

- Should 2c be either OR? Couldn’t it just be RPL value accrual and the %s adjusted as needed?

Potential alternative protocol revenue split, all paid in ETH:

a) 10% (71.42% total revenue) to NOs, irrespective of RPL stake

b) 3% (21.42%) to RPL stakers, do not have to be NOs

c) 1% (7.14%) to RPL value accrual

(haven’t put much thought into the split here)

Re: RPL value accrual (buy+burn or buy+lp):

- What factors determine the split here?

- If buy+lp, what happens to the earned lp fees?

Re: RPL issuance reduced from 5% to 1.5%:

- How will the 1.5% be distributed?

- Is inflation still needed / can it be reduced to zero?

2 Likes

For Saturn 1 we’re starting at 5% to NOs and 9% to staked RPL.

To hit your questions:

- They’re not separated. The 5% is not to ETH-only NOs, it’s to all NOs regardless of RPL stake.

- The most important reason is that aligned governance is important, so there is value to paying for voter_share (vote-eligible RPL staked on nodes). Some of the alternative value capture options for Saturn 2 (buy+LP and buy+burn) do reward all RPL, not just staked RPL – if you want to reward all RPL holders it’s more efficient to use a method like this than to require folks to stake and claim (which costs gas and limits your ability to use RPL for other things).

- Not sure I understand. Are you asking if it could be 5%/9%/0%? Sure? But at that point why bother coding the 0% stuff. In effect, if a share gets to “negligible”, I suspect we gain more from enlarging another share instead.

I won’t respond to your split cuz I think I addressed several assumptions leading you there above.

Value accrual Qs:

- What split? I think we’d only implement one of LP or burn if that’s what you’re asking.

- Fees would do the natural thing they do – the DAO’s LP position would be enlarged by them.

Issuance Qs:

- This is a non-change, we currently distribute 1.5% issuance to the GMC (grants and bounties), the IMC (liquidity incentives), a reserve treasury (misc, most notably including dev team), and the oDAO. The pDAO votes where these funds go.

- We do still have the expenses I noted. It’s possible the levels change over time (eg, we might remove enough oDAO duties that we can be confident gas costs don’t lose them money with a smaller cut). If we do something like burn or LP, the net effect might hit 0% (or less).

Thanks.

For Saturn 1 we’re starting at 5% to NOs and 9% to staked RPL.

This seems back to front. Shouldn’t the protocol incentivize NOs above all else?

Saturn 2 (buy+LP and buy+burn) do reward all RPL

Yes, however, it’s much more abstract and a lot more difficult to assess ROI. I surmise there’s a lot of people who like to stake and earn/claim. Earning ETH too is a powerful incentive (ref. GMX staking).

… there is value to paying for voter_share (vote-eligible RPL staked on nodes)

Assuming anyone can stake, I think staking rewards should be the same irrespective of where staked. From a vote standpoint, RPL staked on nodes can carry a higher weight.

Not sure I understand

See Introduction to the Tokenomics Rework | Rocket Pool Improvement Proposals

“I may benefit from value accrual to RPL (4% of borrowed ETH revenue from all megapools) or from this revenue being used to increase the rewards for staking RPL.”

Perhaps I’m misreading the above. I interpreted it as: 4% of borrowed ETH revenue will either be used for value accrual to RPL OR to increase the rewards for staking RPL?

Noted on inflation, thanks!

From a vote standpoint, RPL staked on nodes can carry a higher weight.

Currently only RPL staked on nodes carry any weight. If RPL is not staked on a node it is not eligible to vote. It is therefor also not eligible to receive voter_share rewards (because it is not eligible to vote).

Why Rocket Pool decided to make only make RPL staked on a node up to 150% of nETH eligible is outside the scope of this rework, but it mostly comes down to NOs (participating in staking ETH for the protocol and staking RPL) are the most aligned with community health. If you remove either of those factors they become less aligned.

You could certainly debate this more and try to change things, but it also doesn’t really fit here since the rework doesn’t affect it.

it’s much more abstract and a lot more difficult to assess ROI.

It is more abstract, yes, but it has benefits that outweigh the abstraction. ROI is actually fairly straightforward: If you own 10% of all RPL and 10 ETH is used to buy and burn RPL, you have received ~1 ETH in increased value of your tokens. There’s always price fluctuations due to liquidity and the market, but the ROI is pretty straightforward.

It has the added benefit of being taxed at a lower rate.

Expect there to be discussions on surplus_share and the effects it has in the near future.

This seems back to front. Shouldn’t the protocol incentivize NOs above all else?

We certainly want to incentivize NOs enough that they want to stake, and we want it to be sufficient that all rETH is staked effectively. That’s why we’ve designed the rate to change rapidly to find the right level. Many people expect the node operator commission to rise rapidly after release to around 7%.

1 Like

Shouldn’t the protocol incentivize NOs above all

Current state: (8+24*.14)/(8+2.4) = 1.09x solo apy

At 5% commission in Saturn 1: (4+28*.05)/4 = 1.35x solo apy

Saturn 2 is even nicer as lower bonds kick in.

Essentially, the current RPL requirement works kinda like a roundabout fee to RPL (tho badly); this makes it less roundabout (and slightly lowers it, fwiw).

Most importantly, UARS is all about listening to the market. We will pay NOs more if that’s needed to attract them.

much more abstract and a lot more difficult to assess ROI. […] Earning ETH too is a powerful incentive

I agree it’s more abstract. ROI long terms is roughly the same whether earnings are direct revenue or indirect accrual (in some jurisdictions, taxes might hit different). The ETH earning bit is a very fair point – being direct makes the value more predictable – this is one reason some folks favor “voter_share” as the primary accrual method.

I think staking rewards should be the same irrespective of where staked.

Yeah… this doesn’t make sense to me. The protocol should pay for value that it gets. Generating governance security and RPL demand is better for the protocol than just RPL demand.

I interpreted it as: 4% of borrowed ETH revenue will either be used for value accrual to RPL OR to increase the rewards for staking RPL?

Yes – there’s a subsequent vote to decide how we want to spend. It’s a little tricky to have an explainer capture multiple options.

2 Likes

Just to keep this thread updated. The discourse sentiment poll was heavily in favour after 14 days, and has now been closed.

Per the outcome, a snapshot vote is now live, and can be found here. Make sure to get your vote in!

The snapshot vote will conclude on August 22nd, two weeks from now.

In order to vote, you will have needed to initialize your voting power post-Houston and prior to the the start of the vote. There’s a guide on how to do this so you are not left out of future votes.

Using this post to log my rationale.

I’m voting for.

The rework is “good enough” from where I stand, though I have some small concerns with the flexibility of surplus share.

RPIP-46 describes 3 categories that revenues can be split into: rETH share, a category based on vote power (pre-sqrt), and a category to pay node operators their commission. It makes somewhat vague mentions of a surplus mechanism.

I would prefer for the UARs RPIP to more explicitly state that it is the “first pass” in a series of splits, and leftover (surplus) revenues will be split according to downstream RPIPs.

I am specifically concerned with leaving the door open to non-linear or piecewise reward distribution curves. At the moment, I am a supporter of one of:

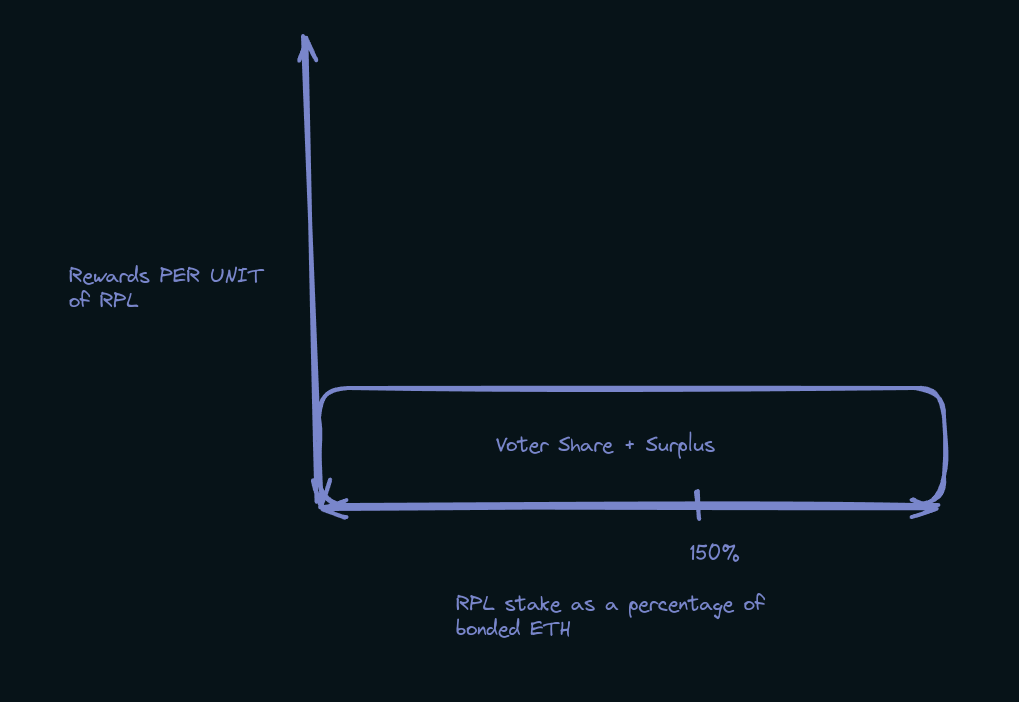

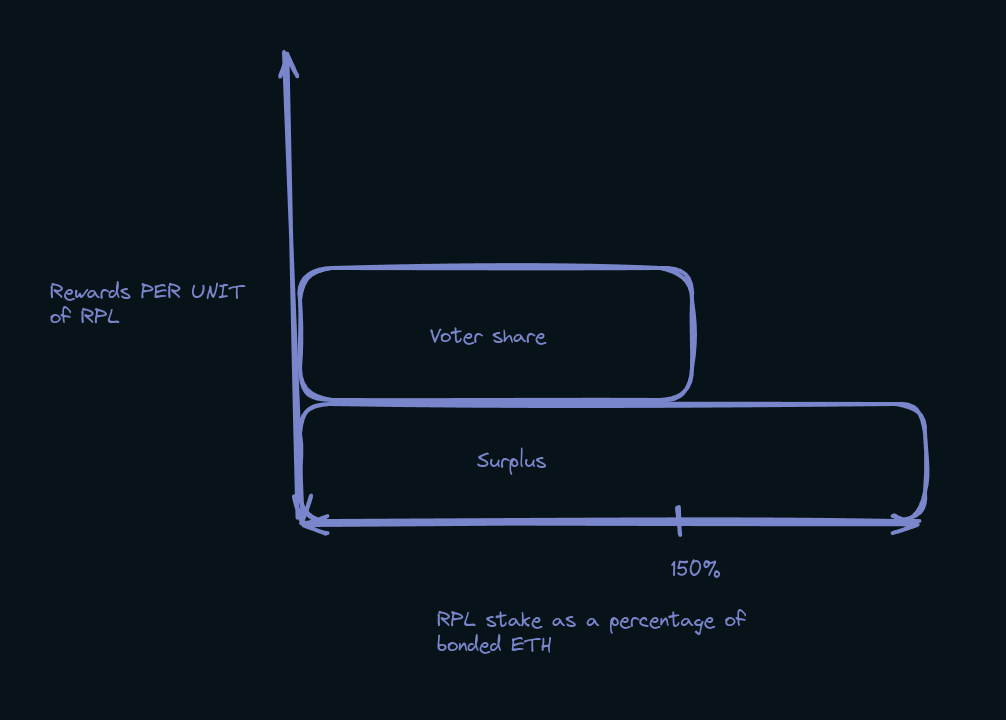

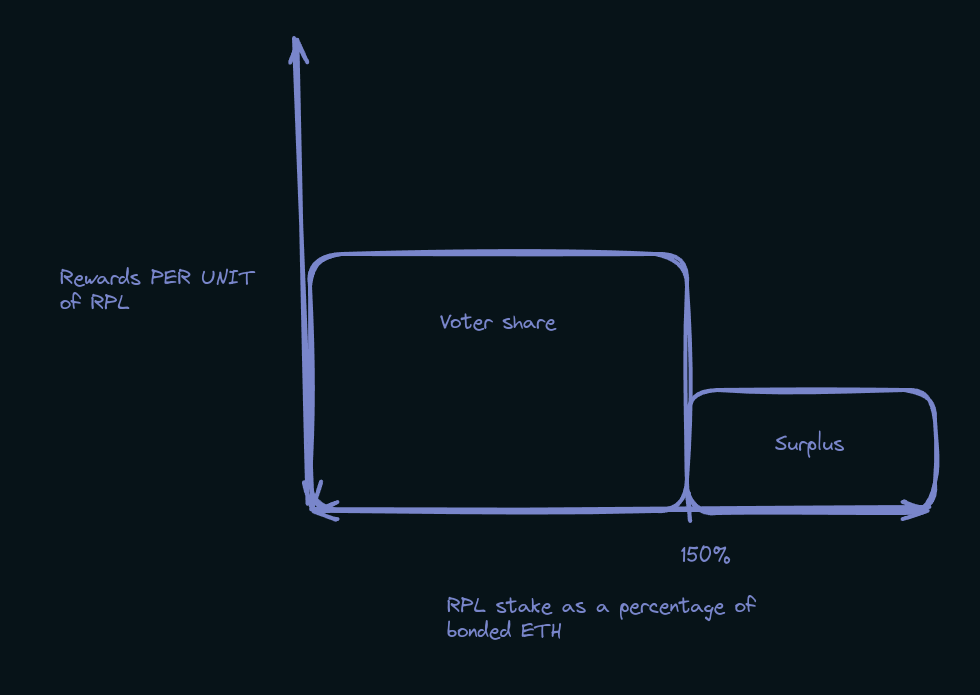

NB: In the following graphs I intended the y axis to be “per additional unit” but I failed and now I’m too lazy to fix it.

surplus revenue being included in voter share, and removing the 150% bonded eth limit to vote power. Vote power is still subject to sqrt, and revenue share per unit of staked rpl remains constant for the entire domain.knoshua convinced me offline that this creates perverse incentives

- surplus revenue being distributed to all node operators with staked rpl directly proportional to their staked rpl (a piecemeal function with two constant curves above and below 1.5)

- surplus revenue being distributed to all node operators with staked rpl above the 1.5 voting power limit, directly proportional to their amount of staked rpl in excess of 1.5

I acknowledge that 2/3 are largely the same outcome. I think I’m happy with 1 as “good enough” but believe 2/3 merit research and discussion. They have downsides, so 1 may turn out to be the right option, in which case, these RPIPs are good as the vote cap can simply be lifted to UINT256_MAX wei. However, should options 2/3 be beneficial, we should leave the door open to them with these changes. I currently believe these changes do that, but it is certainly more of an implementation detail than not (ie, if rewards are to be destributed by merkle tree, we retain full flexibility).

Future vote spoilers: I am unconvinced that the “buy and” options for surplus merit the technical and financial risks they pose and am highly skeptical of them. Non-staking RPL holders will still have avenues to potentially earn rewards for their RPL via wrappers, such as rocketlend and nodeset, but with the base protocol unencumbered by the associated regulatory and technical risk.

2 Likes