We at 1kx appreciate the community’s initiative to improve Rocket Pool’s positioning in the staking landscape and wanted to share some thoughts on the proposals highlighted above.

We believe that proceeding with select proposed RPIPs will allow the protocol to scale effectively without compromising security and decentralization:

- RPIP-42 and -44: Both allow for greater node operator capital efficiency which has been shown to greatly help scale TVL in the past, and forced exits allow Rocket Pool to remove malicious or inactive node operators that would be hampering protocol performance

- RPIP-43: This upgrade helps with gas efficiencies for node operators, which drives down supply-side costs and improves margins

- RPIP-46: We are excited about an adjustable and programmatic splitting function that distributes to various targets depending on protocol conditions and is managed actively by pDAO. For example, when the supply side acts as the bottleneck for more TVL, and there is a deposit queue, commissions can be increased to entice new or existing operators. We are also fully in support of reducing RPL issuance from 5% to 1.5%

Certain other proposals and aspects require careful community evaluation, as their cost-benefit dynamics are far more complex and necessitate thoughtful decision-making.

The Universal Adjustable Revenue Split (RPIP-46) will be a critical new protocol component and deciding how to balance rETH commissions has many implications. In addition to evidently directing revenue to node operators and rETH holders, the initiatives surrounding RPL Burn and RPL Buy & LP warrant deeper discussion. Regarding the former (RPL Burn), we have concerns due to the poor track record observed in the web3 space for similar implementations. Some previous examples include:

-

DXD: The DAO implemented a buyback and burn strategy and acquired 30% of the entire supply costing $8 million in ETH over a 16-month span. The protocol ultimately suspended the program and subsequently established a working group to establish a different path forward. A few years later, the token is down more than 45% since the program stopped.

-

MakerDAO: Maker burned 2.78% of its supply over the course of 16 months between November 2020 and February 2022 but, despite doing so, underperformed index assets like ETH throughout that time. The total spend was $55.8 million, which is multiples larger than what Rocket Pool would potentially burn in one year. Please see a chart of $MKR’s price vs $ETH during the time of burn.

-

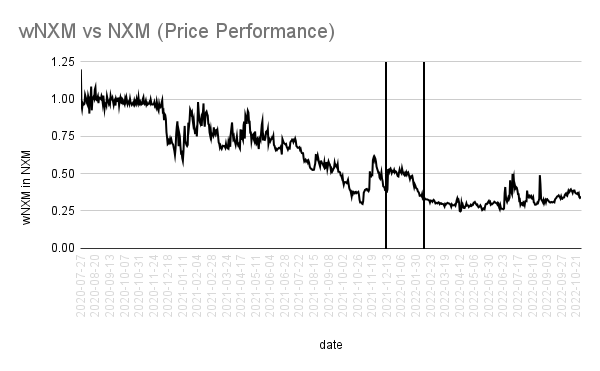

Nexus Mutual: The DAO spent 8,000 ETH or $36 million at the time to try to help WNXM, a liquid version of NXM, trade at 1:1 parity. The buyback was executed between December 2021 and January 2022. One year after the buyback was completed, the initiative never came close to reaching its goal. In fact, for five months after the program, the WNXM to NXM ratio actually reached all-time lows and did not spend any considerable time above 50%, which is what the ratio was before the buyback program.

We would be excited to discuss any positive examples that the community presents where the burn mechanism has brought forth meaningful benefits to a protocol. In addition to poor web3 case studies, we are wary of implementing buyback and burn for a few reasons related to Rocket Pool’s current state:

- This proposal is effectively equivalent to share buybacks in web2, which are often performed for very mature companies looking to return capital or “value” to shareholders. We believe that Rocket Pool has plenty of room to grow, especially considering its market share compared to other liquid staking protocols and the 22% self-limit rule.

- A buyback program might be more impactful when TVL has grown many multiples from here, as the immediate implementation of a buyback and burn would have little effect on the token price: the proposed burn portion, based on current TVL and ETH yields over a full year, is only equal to about 1 day of RPL trading volume or 1% of the $RPL market cap. Protocol ETH should be used to fund future product and adoption initiatives.

- Buybacks are also used to temporarily prop up share price. There may be some perceived benefits to this, such as increased morale in the community, attention from outsiders, and ultimately speculative capital, but the key point is that this mainly benefits short-term mercenaries who are unaligned with the ecosystem instead of those who are long-term aligned.

- Burning $RPL benefits everyone in the ecosystem equally, including those who do not actively contribute to the ecosystem. In other words, burns attempt to capture value when the protocol should be trying to create value, such as by increasing TVL. The main way to create TVL is to give resources to those who are pushing the protocol forward, such as node operators or those doing active BD with new staking partners. Allocating resources to these types of participants is especially important in growth mode.

One thoughtful alternative proposal to burning $RPL is providing liquidity alongside rETH in a 90/10 Balancer pool. This would create deeper liquidity for the $RPL token and can help reduce the overall cost that node operators pay when they are newly purchasing or re-upping $RPL collateral. However, we remain cautious that this would be the best use of funds for a few reasons:

- The additional revenue surplus directed to this 90/10 liquidity pool is not significant enough to drive net new demand for rETH or RPL because all other things equal, there are other liquid staking solutions that will always have deeper liquidity on both their LST product and native token. If users really valued liquidity depth as their number one priority, they would have left the Rocket Pool ecosystem regardless of whether the 90/10 pool was slightly deeper. Increasing the TVL of this pool by a few million dollars will not entice a current Coinbase or Lido user to switch their ETH over to Rocket Pool, nor will it meaningfully affect a new ETH holder’s decision to stake with Rocket Pool.

- Although this proposal would help improve the user experience incrementally through improved swapping rates, directing revenue towards growth initiatives can eventually deepen liquidity organically due to the natural PMF flywheel, where more adoption leads to more swaps, LP fees, and, therefore, liquidity.

- We expect that once $RPL delegation is implemented, operators will use this method to create new validators rather than acquiring $RPL on the open market, thus lessening the value proposition for them. Moreover, deeper $RPL liquidity does not significantly affect an average rETH holder’s experience.

Additionally, we believe that the potential removal of the $RPL collateral requirement should be further discussed and considered. Although there is certainly friction that a node operator undergoes in order to acquire $RPL, and we have talked to several node operators who will not touch the ecosystem because they do not want $RPL price exposure, but there are several positives about this collateral requirement. It attributes intrinsic value to the token, which in turn helps the ecosystem thrive. Moreover, staking is the most proven and best-known token sink in the space and we shouldn’t be shying away from an innovative solution that Rocket Pool as a protocol originally pioneered.

Rocket Pool consistently trades at a premium compared to competing protocol tokens due to this token sink – almost double the [Market Cap / TVL] ratio as players such as Lido, Stakewise, Stader, and Marinade. We believe it would completely disappear if the $RPL requirement was removed. Some considerations:

- Without the $RPL collateral requirement, the incentive to hold $RPL is weakened, which decreases the buy-in of those invested in Rocket Pool’s health.

- We believe that delegation will solve all the problems surrounding $RPL friction for node operators. Delegation allows $RPL holders, whether it be institutional investors or community members, to earn active yield on their holdings in addition to price upside. This replaces the need for node operators to buy or hold $RPL themselves. A delegation marketplace can emerge, enabling competitive dynamics around $RPL staker and node operator commission splits.

We are excited about many of the proposals being presented and look forward to engaging in more in-depth discussions on the more contentious elements.

To aid these detailed discussions, we are currently preparing several new mechanisms that can be integrated into these proposals and are excited to hear the community’s feedback.

It’s crucial to recognize that conversations within the Rocket Pool community don’t frequently reach the wider ecosystem. One of the main aims of our soon-to-be-presented mechanisms is to boost Rocket Pool’s rETH branding in the crypto space, thereby promoting broader adoption.