I wrote the poll to “get a better feel for where the community is at”, but not to be an official sentiment poll directly tied to RPIP vote. Sorry for the confusion…

The forum post had been live for 10 days and had only generated one comment from the community. The goal was just to drive greater awareness and discussion.

Personally I like Scenario B with the 3 releases so that we can get some change happening sooner rather than later.

I’ve only read RPIP 49 in detail, and just a quick scroll through the other linked RPIPs.

Although Scenario B has arguably the most critical component “Bond curves” in its last release, I believe this is unavoidable, as all the other scenarios do the same.

I lean towards Valdorff’s opinion and I make him my proxy for what that is worth.

Rocketpool should focus on safely minimizing the ETH bond required to spin up a minipool.

I have an idea about how we can get this to safely become very small. Research in work.

The RPL burn is nearly meaningless.

This will delay or prevent NodeSet from launching.

Let’s K.I.S.S. and focus on continuing to drive down the ETH bond required to spin up a minipool and reduce Node Operator’s dependence on RPL’s return as a token with LEB4s.

This is a problem with the price of RPL, not with the burn mechanic. If we ignore taxes and unstaked RPL (which will be minimal at maturity), they should yield the same price. When we include taxes there is a clear winner.

I bought a flip phone a few years back - only to have the new 5G networks drop support for them last year. Believe me - I like things to work forever on my own terms too.

As a node operator (and owner of quite a bit of RPL as a result) here’s how I’m thinking about the optional upgrade component.

Curious what you think:

1) Would universal adoption of upgrades make us more competitive as a network and protocol?

Likely. And even more likely if our governance is strong, and talent stays on board. Doesn’t seem likely we would vote and build upgrades that are net negative. What’s good for protocol is good for my RPL, so seems good.

2) Would upgrades cost me money?

Yes, but depends. Gas isn’t free (cough, only kind of regret chasing a sub 100 Minipool ID), but upgrades likely to open doors for efficiencies and ways to make more ETH. So, bad and good; maybe more good assuming upgrades are bread.

3) Will some Node Operators likely get blindsided by an upgrade (even with ample time to upgrade) because they are “set it and forget” operators?

Yes, and this isn’t great. I believe we’ve seen quite a long tail on smartnode upgrade adoption, and voting participation. And we’ve seen a few cases of nodes suffering for weeks of missed attestations before wising up.

Makes me concerned some may not know and miss the boat on upgrades. Even if those absent node operators were mediocre/poor performers (I haven’t looked to see if there is a correlation between beacon rating and smartnode release/gov participation) it doesn’t feel good to see people’s nodes shut off or flounder.

Perhaps a community project could focus on alerts in general. Improve node operators awareness of upgrades, smartnode changes - only the very important notices. I know there are many sources (beacon, discord, Twitter) - but there is also a LOT of noise in all those sources too, not just the most important thing for node operators specifically.

4) Node Operators are stakeholders in the protocol itself - not only users. How do you balance the trade offs between what’s good for you, and good for the protocol?

For me, it’s clear I forego some control with this change component, which I don’t prefer as a user of the protocol. But overall it seems net positive for the protocol itself, so as a steward and stakeholder I am on board with it. I’ll note - I really think it all hinges on our ability to retain great talent and prioritize strong functionality via governance, as I mention in question 1.

As far as Scenario preferences - I’m in favor of moving fast. If breaking components into releases helps us ship faster, we should do that.

I’m most concerned about our ability to competitively attract new Node Operators, so I don’t mind the extra benefit ETH only Node Operators would get in Scenario B. Extra juicy for those solo operators who shift over right away.

Will RPL Burn create more value for RPL holders than if they were to convert their RPL to ETH and spin up new minipools using said ETH? I fear a RPL sell off race if this is released.

So I support the new tokenomic ideas in large part. My thoughts regarding why the current system will not be successful:

With LEB4, current tokenomics suggest a 9% benefit in ETH terms over solostaking; LEB4 will give us ~ 16% benefit over solo staking. Lido CSM initial modeling suggests a 50% benefit over solo staking, without requiring any other token investment. And that’s before Lido discusses things like subsidizing CSM from its legacy operators, or shifting payment structures to squeeze out competition. It’s not just that we aren’t competitive, current tokenomics are hardly even playing the same game.

In the last year, essentially everyone who became an LEB8 node operator has LOST money in ETH denominated terms. The return on RPL is based on the willingness of people to buy it in order to get more ETH- even to get inflationary rewards the price of RPL has to remain stable or rise. I cannot ethically encourage people to buy if the tokenomics remains the same because i personally think the most realistic outcome is that the bleeding will continue. With the new system, no one needs to buy RPL for it to gain value.

While I understand the impulse to first maximize the benefits of bond reduction, in order to expand with our current tokenomics we need absurd amounts of collateral. For instance, the proposed SamDoff tokenomics posits LEB 1.5. Under current tokenomics to get this level of benefit you would need a minimum RPL bond of 3.05 ETH (200% of your bonded ETH; >2/3 of your stack needs to be RPL). There are only a handful of people this applies to, and rather than decentralizing the protocol with lower bonds it would high centralize it. There are many of us who felt 10% of protocol ETH was too high a ‘price’ to become a NO; I think that we have given enough time to prove this concern correct, and RPIP 8 specifically prepares the DAO for correction if the assumptions about being rETH constrained do not pan out. https://discord.com/channels/405159462932971535/774497904559783947/1035537700515762197

I sympathize with the concern that tokenomic changes seem like effective rugs to investors who counted on a particular set of variables. However, as someone who invested on the way up (up to 0.02) and on the way down (from 0.02 to 0.008xxx), I will make the opposite point. I did not invest in the current tokenomics; I invested in the belief of problem solving by the team and the community to conquer anticipated and unexpected problems. I think this is true of many investors; you don’t invest in “what is”, but what “could be”. Or you don’t invest in the product, you invest in the people.

NodeSet is highly RP aligned, and from its genesis as the Node Operator Association it has had the interest of NOs and Ethereum at heart. These changes may significantly disrupt Constellation, which is very unfortunate. However, it is too risky to put the future in the protocol in a third party when we can make changes ourselves: the expected demand may not materialize; the contract could be faulty; and it’s just a bad look for a permissionless/decentralized protocol to be so reliant on a centralized service to survive. Waiting another 6 months before considering making changes will really leave no time to respond to CSM.

So I would oppose almost any plan that consists of “mostly keep current tokenomics”.

Some parts I would like to see changed in the SamDorff proposal:

I would like to see the pendulum start with higher payments to NOs with a ramp down (rather than lower ‘voter’ share that will likely ramp up) for more quick market share growth of validators. That may cause short term volatility in the speculative market, but would be continue to make marriages and for example NodeSet still very relevant. Overall, I think a higher proportion of RPL can be safely staked (would be ok with up to ~95% staked)

Excepting this, I prefer keeping inflation to NOs in RPL, rather than distributing ETH to voters (ie 100% of non-rETH/non-NO commission goes to buy/burn)- at least for now. This provides greater continuity to the current system, and can be changed later once we feel comfortable that our system has stabilized.

Honestly, this was a pretty disappointing read. There were over 2 pages dedicated to trashing RPIP-30, which is unrelated to the current proposal. I can only assume the point of this is to discredit me personally, as having had a significant hand in authoring that RPIP. FWIW, the core of the attack is that ratio went down after it. Correlation is definitely not causation. For example, lets add another important RP milestone (blue lines are pDAO/oDAO charter and oDAO inflation reduction). I would argue that (a) it was a more impactful change than RPIP-30 and (b) it lines up with price changes more. Do I believe it’s responsible for that drop? No.

The biggest issue I’ll note with this writeup is that it doesn’t present an alternative path that will actually provide significant growth – it just assumes growth will happen: “In short, there is significant growth potential for the RPL/ETH ratio under current tokenomics, assuming the protocol can achieve the required TVL growth.”.

There is very little justification for significant growth under current tokenomics. It is based on:

LEB4s (I agree that this would have some impact)

Full migration to lowest bond; despite evidence that we don’t get full migrations and an even higher RPL exposure

In a couple of places, lowering required RPL is suggested as a temporary measure, including by 4x. It is not stated why we would expect this would be temporary, and the valuation table does not include this impact.

The floor model which is based on topping off; despite evidence that many do not (and some even exit minipools)

What if we kept current collateral-style minipools around? And add an additional class of eth-only pools that receive a lower commision and the rest goes to burn?

This way:

rpl-holding NOs get rewarded with full commission

nodeset gets minimally disrupted (as it should be more attractive than eth-only minipools)

eth-only stakers can still participate and outperform solo staking

To avoid a completely separate class of pools, maybe NO commission can scale from “eth-only” to “full-commision” depending on rpl staked? Or use the current hard threshold to treat pools below staked threshold as eth-only pools.

@samus originally had something along these lines described as “boosted commission”. I do like that your version has a fixed amount of revenue going to RPL, either via burn or via commission boost, so modeling is not a total nightmare. That said, I think this remains a lot harder to explain than simply splitting revenue (essentially a pie chart).

Also, it’s not clear why we’re paying RPL stakers more here… what additional value are they creating? In the current proposal, there is a slice that goes to vote-eligible staked RPL, for governance work, but there’s a heuristic that essentially has a preference for unstaked RPL (which can be used to generate exogenous value for holders) once “enough” RPL for governance is staked.

I don’t have a strong preference on the voter share’s starting point. I do think 95% is significantly more than needed. It’s not about “safety”, it’s about maximizing ecosystem value. By definition, staked RPL is idle and cannot generate exogenous value for its holders.

My point is rather that I believe a RPL-staking NO is contributing significantly more to the protocol than someone that is purely staking RPL, and should be rewarded. A separate slice for vote-eligible RPL does this to some extent, but I believe my suggestion is a much smaller change from current tokenomics.

Basically you could pitch it as:

megapools, leb4+1.5, etc (all the goodies proposed above!)

RPL requirement removed for minipool creation

Commission scales from min%-max% based on eth value of staked rpl / borrowed eth. Remaining commission is used for buyback+burn.

Current state is equivalent to full commission at 10%, but we could experiment with this number. If we set it insanely high my idea basically reverts to the current proposal of full burn

This would also encourage people that are on the fence to start as ETH-only and slowly increase their RPL position as they grow more comfortable and want to unlock more yield on their minipools. I think the psychological effect of earning access to your yield, rather than protocol yield is quite strong (but of course purely anectotal)

An interesting effect is also that if RPL price drops, the buyback naturally increases to counteract the drop.

There were over 2 pages dedicated to trashing RPIP-30, which is unrelated to the current proposal. I can only assume the point of this is to discredit me personally, as having had a significant hand in authoring that RPIP.

Let’s keep this professional – we are talking about ideas, not people.

That section is inside Part 1, an overview of the existing state of RPL, which is important context for the proposal. Here, we are presenting the data we’ve gathered from the hundreds of conversations we’ve had with RP operators in our community. This seems like pretty valuable qualitative data for the RP community to consider, but although it’s certainly statistically significant, it’s not conclusive. To quote the introduction to that section directly:

“Our research suggests that RPIP-30 may have a downward effect on the RPL/ETH ratio by incentivizing lower average collateralization. However, more conclusive evidence is needed to justify this conclusion at scale, and the magnitude of this effect is difficult to quantify beyond the hundreds of thousands of RPL represented in our conversations. We present it nonetheless for completeness.”

The biggest issue I’ll note with this writeup is that it doesn’t present an alternative path that will actually provide significant growth

The point of this document is to study the current tokenomics situation and analyze the risks of these proposals for RP and our own community – not make formal proposals for change (that’s the job of RPIPs).

That said, I see several paths to growth for RP without dramatically altering the current tokenomics:

LEB4s, like you mentioned, are a proven method. The TVL roughly doubled before flattening again after LEB8s were introduced, even without full adoption. Maybe because people saw growth and jumped on?

Constellation will of course unlock the NO side of the equation while giving users more incentive to join RP. This requires no changes to the base protocol, but the changes suggested here will hinder it.

Many of your own suggestions can work side-by-side with existing tokenomics. If ETH-only minipools are limited to 10% of TVL (the amount that Lido believes is the maximum safe level), that could provide up to 10% growth as well. As outlined in the report, however, we can’t recommend moving to ETH-only minipools at a large scale given the significant centralization risk.

All in all, I think it’s worth taking a step back and digesting the document for what it is: a review of the current situation and a risk analysis for proposed changes alongside some recommendations which come from this work. Nothing more, nothing less.

Hello,

so I read the proposals and have a couple of questions for clarity:

Why are you saying that 5% commission is generous when we’re getting the full 14% commission now? Why would I as a current node operator want to get less?

If RPL is no longer needed to operate nodes, what’s the point of buying RPL?

If RPL is no longer needed to operate nodes, but allows the holders change what a node operator earns, how can any node operator ever trust RocketPool? (UVC)

Posting here because because I don’t github. Essentially this proposes a few tweaks to the current tokenomics thread. Bond curves, megapools, forced exits, UVC will be unchanged. It’s kinda rough, so my apologies:

The basics are:

Each node collects a NO fee from the rETH share for performing validation duties

Each node collects a governance fee from rETH proportional to its governance power

The NO fee is variable based on relative demand for NO:rETH

NO inflation is variable based on relative demand for staked:unstaked RPL, with goal 0% overt time.

Nodes with higher relative staked RPL get preference in the minipool queue

Direct capture (voter share)

This is the governance fee changed to rETH. In my proposal it will be set at 100% of direct fees (or 11.5% rETH commission) for the foreseeable future and is not variable until RPL inflation to NOs is 0%.

Direct capture (RPL Buy/Burn):

0% of direct capture will be directed to buy/burn (or other similar mechanism- like LP etc). There is however, no reason this could not be set at 100% governance fee for instance, or to go halfsies; once staked % is higher I might favor change to buy/burn. But i think ‘voter share’ is simpler to start and avoids some perceived issues with rewards going to a majority of unstaked holders.

Inflation

I propose this be a dynamic inflation with % to NOs within the previously proposed heuristics; starts at 3.5% and goes -0.5% at given time if staked RPL % is greater than a given heuristic.

Validator queue order

One of my major takeaways that i got from the Atlas transition was that we wasted a LOT of gas fighting each other. When there is a minipools queue, having more minipools in the queue does not help create more rETH nor does it help anyone get through the beaconchain queue faster. During Atlas, people were spinning up minipools at 100 and 200 gas because they wanted to get in front of other NOs. This internal warfare is pure waste, and the gas used leaves the protocol. This is opposed to spending significant gas to get into the beaconchain queue, which at times may be net positive for both the protocol and the NO.

I propose using a different ordering system which is not first-come, first-serve. In it, nodes in the queue with the highest staked RPL/protocol ETH would be chosen next to stake. Rather than spending money on gas wars with each other that simply leaves the protocol, NOs spend money on staking RPL which benefits the protocol. They have a built-in incentive to wait for cheaper periods of gas to make transactions, keeping more money in the protocol. This also gives a benefit to those who have previously been stakers with rocket pool for migrations. It also give a benefit to people spinning up their first two LEB4 (since they will require ~70% less RPL per ETH staked to spin up minipools). Lastly, it will relieve the concerns of Governance capture by a large number of non-RPL bonded minipools clogging the queue; they can always be jumped by folks with >0 RPL bond.

There is certainly the possibility of buying RPL, jumping the queue, waiting a month to unstake, and selling it. However, this is very unlikely to be more cost effective than just waiting, and obviously if the NO ever wants to spin up more minipools they might have to do the same process.

Governance accounting:

There are concerns expressed in this forum about both the direct capture idea in general, and also specifically the buy/burn. I think this is mostly a optics issue because to me it is clear that the RPL direct capture is a payment from rETH, not from other NOs, not from others’ efforts, but rather a fee FOR governance efforts. I think that is more clear in buy/burn when a higher proportion of RPL is staked (85% let’s say), so that the preponderance goes to people who are running nodes and governing.

However, I think it is reasonably easy to separate the accounting to make it clear who is paying whom. Rather than splitting the governance fee (direct capture share) from all NOs, i propose it is taken proportionally from rETH as a fee by the NO which is doing the governing; in my proposal that fee is kept by the NO, although through governance that fee could do whatever the DAO wants (buy/burn etc).

You need the following ingredients to determine splitting:

NO fee %

total RPL staked

RPL staked in a node

approximation of the ETH earned by all rETH in a month

governance fee%.

So for example, let’s say your NO fee was 2.5%, your protocol wide rETH fee was 11.5%, your total RPL staked was 10,000, and your approximate ETH earned across all rETH share was 10E for the month.

On next distribute, a RPL node with 0 RPL would distribute 2.5% of rETH rewards to themselves, 10* 0/10000 = 0ETH to governance fees, and 97.5% of rewards to rETH.

A RRL node with 10 RPL would distribute 2.5% of rETH rewards to themselves, 10* 10/10000 = 0.01E to governance fee (in this case, to themselves), and the remainder to rETH

A node with 1000 RPL would distribute 2.5% of rETH rewards to themselves, 1000/10000=1 ETH to governance fee (in this case, to themselves), and the remainder to rETH.

Thus each node is responsible for distributing a fee from rETH proportionate to its own efforts in DAO governance. Likely the easiest would be for the oDAO to record a single value each reward period, and using a similar merkle tree to current RPL rewards each node could prove its RPL staked at snapshot, and the governance fee taken whenever the next distribution happens.

Regarding the approximation of rETH share variable

In this regard, i think a simple approximation is fine. For example, we already track attestations and execution rewards in the smoothie. The approximation could be [total pETH]/[smoothie pETH] x (execution rewards x (#attestations x [constant that approximates attestations to total consensus rewards]).

With 50k minipools, this will likely get us within 1% of accurate, and it’s important to note that because it is a single protocol-wide number, it’s not gamable by individual NOs or rETH traders. If it is consistently off in one direction, that is where UVC provides corrective action.

So combined these changes:

Simplify the scheme by only having only 2 knobs initially (inflation and UVC rETH commission)

Provide gradual encouragement to migrate to megapools as RPL inflation decreases and governance fees increase

Clearly defines who is paying for governance, as ETH only minipools have a pure split with rETH

Adds additional value in RPL in preferentially getting through the queue (keeping some of the value as entrance ticket to minipools), and gives NO a path to pay the protocol to jump the queue during low gas times rather than compete in gas wars

Gives preference for 4E minipools (ie, gets small/new NOs onboarded with less RPL)

Prevents ( edit) centralization risk by large numbers of ETH only minipools

valdorff reply

1:

It makes a strong assumption that 3.5% (not variable) is enough for NOs. If it isn’t, we simply stagnate. I don’t feel we know the market well enough today, and even less tomorrow, to take that strong a stance.

I think either you are misreading me or i’m misreading you. Maybe both. It’s current inflation rewards (3.5%) + all direct capture (100% voter share). Inflating more is not going to create any real value- not sure why you think this would help make more NOs. That’s really driven by NO share, which is governed by UVC (variable commission from rETH)

2:

fine; I might prefer market share as a metric instead of staked RPL

I think my plan is similarly arbitrary but keeps us from adjusting 3 variables at any given time.

3:

This concept makes money flows far more confusing to me. The current proposal takes rETH’s share and splits per the settings. The purported confusion only happens if we confuse what belongs to the protocol and what belongs to the NO. The execution ends up significantly more complex (including requiring an oracle for any distribution).

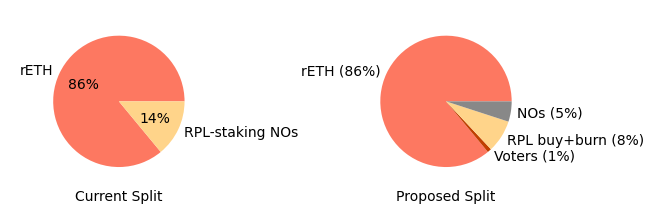

This might be more confusing to you, but it is clear to me that people are worried about regulatary effects of routing NO work to RPL holders. Look at the chart below:

I think the most obvious way to interpret is that a large portion of the NO’s current payments is now going to buy/burn. The rETH portion remains the same. You can talk around it, but as you say a simple chart is worth a lot of words.

Now I 100% agree with you about where this slice is actually coming from- but at the very least it needs rebranding:

A) on the second chart, rETH could be 97.5%; that’s the only chart a ETH-only NO needs to see.

B) on a third chart, split the rETH share; that’s the chart a RPL staker would want to see.

C) ‘voter share’ and ‘buy/burn’ needs rebranding. Not sure how, but something that conveys this is rETH paying for governance/oDAO/pDAO, not a slice from each NO’s share of commission.

I don’t like the complexity of this particular part of my proposal; however, I think as a thought exercise it is useful.

4:

I don’t think this gives RPL much value (eg, it could be sold after skipping the queue), and I do think it has big negative externalities

I agree that it doesn’t a huge amount of RPL value, but it gives some in very specific timeframes (ie, at transition points- nETH highwater mark, initiation of new LEB levels). If there is a queue and I have two NOs, I’d certainly prefer someone able to participate in governance; it’s strictly better for the protocol. This is something only used in rare cases, but taking back just a shade of RPL as entry ticket- a small bone to throw to current NOs because we are changing SO MUCH.

5:

I think favoring early deposits, otoh, is brand-positive. I like these being able to have a priority queue.

It’s a nice thing

6:

We want to avoid being the RPL-washing for a centralized entity. Because of the potential regulatory concerns and price fluctuations of RPL this is of course much less palatable to large organizations seeking consistent higher yield. As with many of these, this is not to address your concerns, but the concerns that have been submitted by NodeSet and others.

I included @Epineph’s unsmoothing fee. I think it’s a great idea that solves MEV theft losses. The downside is that while it’s barely profitable for single-minipool operators right now with bad luck, it could be unprofitable if MEV income goes up and the operator gets low MEV.

I think it likely that if all of the tokenomics changes go live we will be rETH constrained in the short term. To ensure more fairness RPL requirements will be phased out in the transitory phase, ensuring those with higher RPL staked will get priority on the deposit pool over people with low RPL staked

The bonus commission (voter_share ) is proportional to the protocol’s unstaked RPL

UVC uses an on-chain feed-forward PID controller that is able to account for changes to burn rate as well as balance demand in an automated fashion. I do not believe a DAO can balance things quickly enough. I have an algorithm I can propose and tune to do this entirely on-chain, and can do this if sufficient interest is expressed

Responding to @epineph…

1: I think this is a huge issue. It makes a strong assumption that 3.5% (not variable) is enough for NOs. If it isn’t, we simply stagnate. I don’t feel we know the market well enough today, and even less tomorrow, to take that strong a stance.

2: fine; I might prefer market share as a metric instead of staked RPL

3: This concept makes money flows far more confusing to me. The current proposal takes rETH’s share and splits per the settings. The purported confusion only happens if we confuse what belongs to the protocol and what belongs to the NO. The execution ends up significantly more complex (including requiring an oracle for any distribution).

4: I don’t think this gives RPL much value (eg, it could be sold after skipping the queue), and I do think it has big negative externalities (one NO decreasing their queue time uncertainty increases uncertainty for every NO behind them; doesn’t align with bullet 1 or 3 in [pDAO charter] (RPIP-23: pDAO Charter)).

5: I think favoring early deposits, otoh, is brand-positive. I like these being able to have a priority queue.

6: totally confused. They have 0 vote power. Responding to the edit: Hmmm… the premise here is essentially (a) “no big player would hold RPL, even for the time it takes to launch pools” and (b) “we permanently have a queue with RPL holders in it”. I think that’s unlikely to be the case. If this was seen as a big win, a big player could probably figure out a short position to own RPL for a period at quite low risk. If we were committed to this, we’d want to trigger increases in no_share earlier in order to help (b). I guess my question is… if we are trying to avoid taking on ETH-only, why offer it?

a median result of “barely positive” is disastrous optics imo. The closest okish thing I could imagine would be something like requiring smoothing pool participation at low count, and allowing this as an opt out at high count once median return is solid. Implementation is pretty tough, but so is MEV theft stuff. I think I’ll say the same as putting real work into penalties… We need to get something done here, but there isn’t yet apparent urgency based on monitoring so far. I don’t think it’s worth delaying the other tokenomics work needed to get this in.

it’s not clear to me why having more RPL stake is “more fair”. As I noted above, I think this is not aligned with the pDAO charter and not positive for our brand. That said, this is muuuch more palatable to me than Epi’s variant as it’s a single one-time transition, not an ongoing thing. (I’ll grant there’s a benefit to “smooth”)

I think the market take on DAO response vs “magic algorithm makes good decisions” is best shown by comparing early DAI and RAI. My take is that users don’t like ?? rewards (especially controlled by concepts they don’t grok), and prefer defined rewards (even if they can be updated).

Sometimes the right move is qualitatively different, not purely quantitatively different. Eg, we might do more for rETH demand via spendifj on marketing, education, partner incentives for defi usage, etc - as opposed to spending the same amount on rETH_share. A PID controller can’t do this type of thinking.