Hey Everyone!

I’m hoping to propose an alternative tokenomics approach which is far simpler than a few of the other options that have been discussed here thus far.

It is simple to implement, easy to understand, and also allows Node Operators to earn multiples of the Solo Staking APR.

Introduction

I had a great discussion about my ideas in detail with Waq and Samus here (Rocket Fuel - Evan’s Tokenomics Proposal - Samus’ Feedback) on Rocket Fuel and would highly recommend taking a listen!

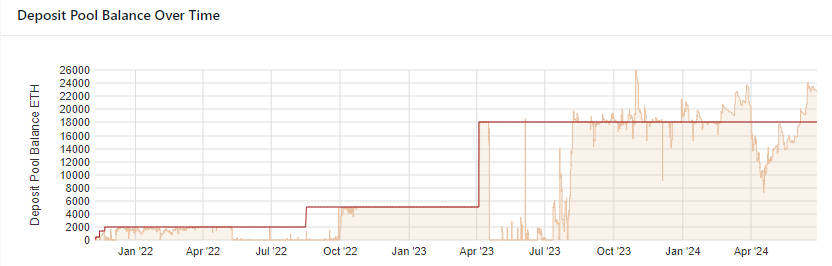

Today Rocket Pool only has about 4% of the liquid staking market. Rocket Pool needs to get serious about gaining market share.

However, Rocket Pool is bottle-necked by the ability for its set of Node Operators to mint rETH.

The market has made it clear that the return for Node Operators is not attractive enough, and too heavily reliant on RPL, which is a highly volatile token. The deposit pool has been full for a significant percent of the time since August of last year. Rocket Pool’s largest periods of growth have been when the deposit pool was not full.

rETH is the product that Rocket Pool sells; Rocket Pool should strive so that Node Operators are never the bottle neck. This also has the added benefit of avoiding the drag on APY the deposit pool has on rETH when it is full.

To solve this, my proposal is quite simple and has two parts:

-

Continue down the LEB curve while maintaining the 14% commission.

- Reduce the ETH bond for Node Operators - starting with LEB4, then progressing to LEB 1.5s with forced exits.

-

Reduce the RPL minimum bond to 10% of Node Operator ETH

Profitability:

A Node Operator’s commission is derived from the borrowed ETH that comes from rETH depositors. This is the primary source of a Rocket Pool Node Operator’s commission. As the eth_bond is reduced for Node Operators, a Node Operator’s profitability vastly increases.

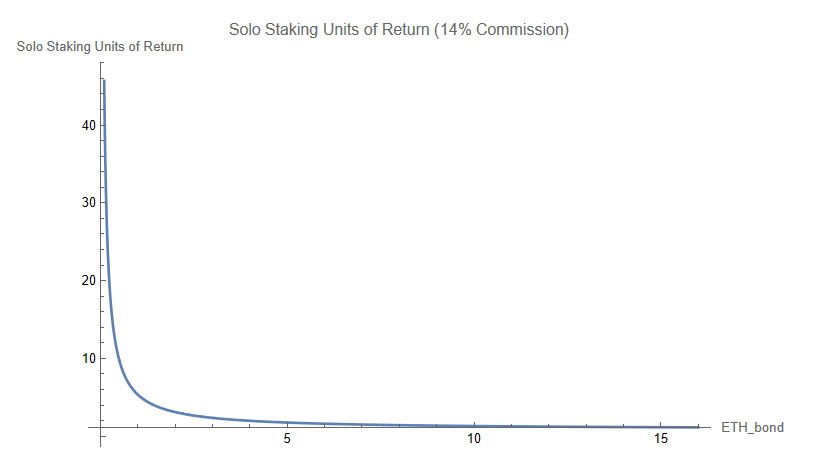

The following graph is denominated in multiples of solo staker APR.

Notably, at LEB4, a RP NO earns twice as much as a solo staker in pure ETH rewards - before accounting for any RPL inflation.

At LEB1.5 with forced exits, a RP NO would earn 3.85 times as much as a solo staker in pure ETH rewards, without accounting for RPL inflation at all!

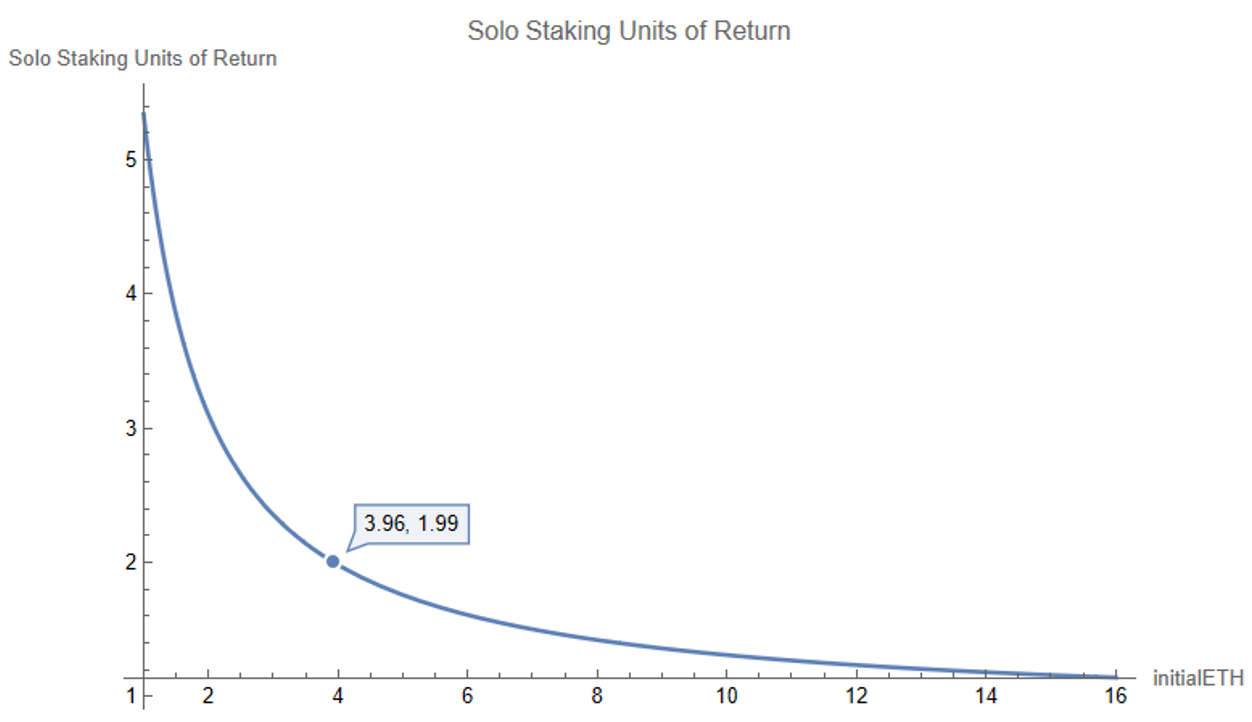

Zooming in on this same graph at the LEB4 position:

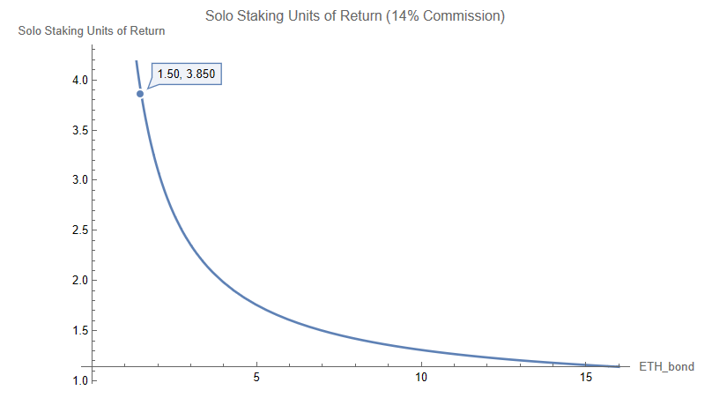

And also on the LEB1.5 position:

A derivation of the math for the above graphs follows:

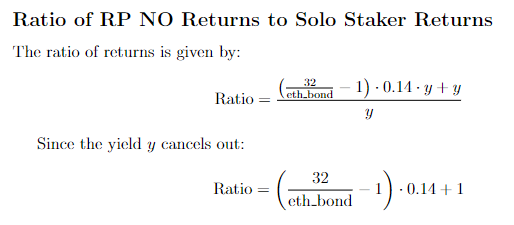

We want to know how profitable being a Rocket Pool Node Operator is relative to being a solo staker on a per ETH basis.

So, that would be the Rocket Pool Node Operator returns, per ETH invested, divided by the solo staker returns, per ETH invested.

Let’s start with the denominator, solo staker returns per ETH invested.

For one year’s worth of returns, we have 32 times the yield, but since we want to know what the returns are per ETH, we divide by 32 and are left with the yield. This makes sense, since that is the definition of yield: returns per unit of account.

![]()

Next, we want to know how much a Rocket Pool Node Operator earns on a per ETH basis.

To calculate this, it would be the eth_bond provided by the Node Operator times the standard staking yield, plus the yield earned by the borrowed ETH multiplied by the commission rate, where the “borrowed ETH” is just 32 ETH minus the ETH provided by the NO.

![]()

However, we want to know how much is earned per ETH invested, so we would divide this by the ETH provided by the Node Operator, which is the eth_bond.

We now have our numerator and our denominator. Dividing our numerator by our denominator, we are left with the following:

Checking our boundary conditions, when the NO eth_bond is 16 ETH, we have:

((32/16) - 1)*0.14 + 1 = 1.14

This is what we expect - we have recovered the 14% commission Rocket Pool Node Operators receive for their 16 ETH bonded minipools.

What about for LEB8s? We have:

((32/8) - 1)*0.14 + 1 = 1.42

Again, this is what we expect - we recover the 42% increased ETH rewards which was used to advertise LEB8s.

How about when the eth_bond is very small, say, 0.01 ETH?

((32/0.01) - 1)*0.14 + 1 = ~ 448

Again, this is what we expect, as per the above graph.

As the eth_bond gets small, the 32/eth_bond term dominates, and the function looks like a 32/x function, where x is our independent variable - the Node Operator’s eth_bond.

Hurdle Rate

Lido’s CSM is advertising at least 50% more returns for Node Operators compared to solo staking. To continue to be relevant in the liquid staking market, Rocket Pool must achieve returns that are more competitive than 1.5x the solo staking yield for its Node Operators,

on a per ETH basis.

As you can see from the above, LEB4 at 14% commission achieves this goal, returning ~ 2x the solo staking return in pure ETH rewards, without accounting for the RPL income from RPL inflation.

Once the protocol gets forced exits, the eth_bond can be reduced to 1.5 ETH, which would increase the ETH denominated yield to 3.85 times the solo staking yield!

Another way to think about the above graph is - on the far right of the graph when eth_bond = 16, it maximizes value accrual for the RPL/ETH ratio.

On the far left of the graph, where we get into LEB range - it maximizes for protocol TVL - while also exposing Node Operators to much more borrowed ETH, and hence ETH denominated revenue.

LEB8 was smack dab in the middle of these two positions - optimizing for neither one.

So what is the tradeoff space that Rocket Pool should be operating in?

Pay Node Operators in ETH by exposing them to more of the ETH yield through borrowed ETH, without overly constraining the size of the Node Operator set. This is the true commission for Node Operators.

If we run out of demand for rETH (this is a long runway, in my opinion) then we reduce the rETH commission from 14% → 10%.

Even at 10% commission for Node Operators, they would still be earning ~ 3x pure ETH rewards compared to solo stakers for LEB1.5s!

Part 2: RPL

The second part of my proposal is to change the RPL collateral requirement from 10% of “borrowed eth”, to 10% of the “eth_bond”, or the ETH brought to the protocol by the Node Operator.

This would represent a reduction in the RPL collateral required for LEB minipools. The reason for this reduction is simple. Node Operators have made it clear that they want to earn ETH, not RPL.

By reducing the Node Operator’s required exposure to RPL, the ETH rewards that I detail above will dominate - making being a Rocket Pool NO far more attractive.

I model what these returns would look like in various RPL performance situations below.

The bottom line is Node Operators would be significantly more profitable in this proposal relative to solo stakers in pure ETH rewards.

So, why RPL at all?

RPL has served, and still would with this proposal, as a “shield” of decentralization for Rocket Pool, to put it a bit dramatically.

RPL would still serve to help keep the protocol decentralized.

This is likely due to ambiguity surrounding legal RPL’s status, and also large corporations’ unwillingness to go that far out on the risk curve by owning RPL, which is a requirement to be a Node Operator.

The result is that quite a significant portion of Rocket Pool’s Node Operator set are home stakers, who have the freedom to invest their own funds however they wish.

The other aspect is governance. RPL still has utility as a governance token.

RPL would retain the same functionality and utility it has today, the only difference is Node Operators would now derive the vast majority of their returns from the commission on borrowed ETH - and not their exposure to RPL.

Would this be negative for the RPL/ETH ratio?

Potentially in the short term, but I do not think so in the long term. Prioritizing TVL growth for the protocol will have a greatly positive effect on the RPL/ETH ratio in the longer term horizon.

Empirically, LDO is worth 5 times as much as RPL in ETH market cap terms. This is likely in part due to holders’ belief that owning LDO is a call option on Lido’s willingness to turn on the fee switch in the future.

The take-away is this: if Rocket Pool had 22% market share - empirically, RPL/ETH ratio would be significantly higher than it is today.

I am not necessarily against turning on the fee switch for RPL - but turning it on today, when the protocol only has 4% of the liquid staking market, would be incredibly pre-mature.

Rocket Pool should instead prioritize TVL growth by maintaining the 14% rETH commission (for now) and lowering the eth_bond for Node Operators, unlocking multiples of pure ETH yield relative to solo staking.

An additional important point is that by turning on the fee switch for RPL, RPL’s valuation would then become sensitive to the ETH staking yield, which will likely continue to compress over time.

The benefit of the proposal that I have detailed above is that it is not sensitive to the staking yield (as long as it remains positive!).

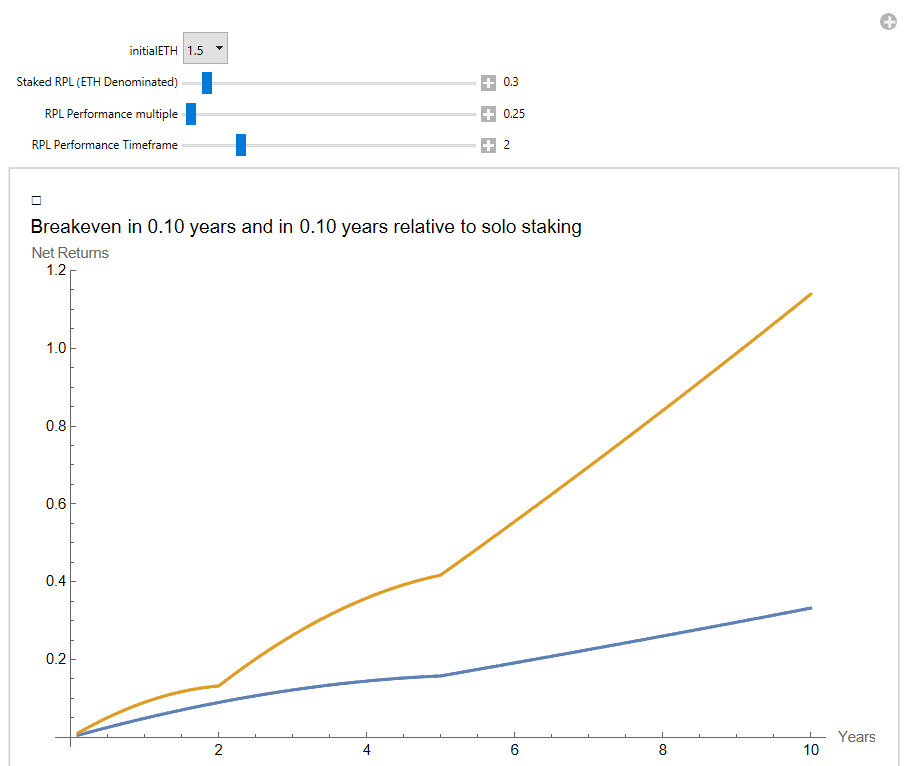

So, what do returns look like for this proposal?

I have put together a model of forward looking returns, denominated in ETH.

I make two assumptions.

The first is that the vanilla ETH staking yield starts at 3.5% and declines to 2% linearly over the next five years, then remains at 2% terminally.

The next assumption I make is that the RPL yield is 8%, which is what it was when I made this tool a year ago, although it has since climbed to 9% today. But to be conservative, I will keep it at 8% for the purposes of the model below.

With that out of the way, modeling is below.

Relative to solo staking, the ETH denominated returns are quite good.

The below scenario is “best case”, where the Node Operator is operating an LEB1.5 and has 0.15 ETH’s worth of RPL staked.

I also assume the RPL/ETH ratio declines by 75% in the first two years of staking.

Despite the RPL/ETH ratio drop, the Node Operator is still significantly more profitable than a solo staker!

(Rocket Pool NO returns in Orange, vanilla Solo staker in blue)

What about if the Node Operator is collateralized at 20%?

Still, the returns are very attractive, even if the RPL/ETH ratio craters by 75%.

The fun thing about this code is that you get to pick the scenario you would like to see and project forwards.

Here is the mathematica code, you can convert it to python using your favorite LLM if you would like: mathematica code

To wrap up:

Rocket Pool should continue down the LEB path by lowering the eth_bond, maintain the 14% commission in order to make being a Rocket Pool Node Operator extremely attractive compared to the Lido CSM, and change the RPL bond requirement to 10% of Node Operator bonded ETH.

~fin~