This is a submission for “Options forum thread”.

Summary

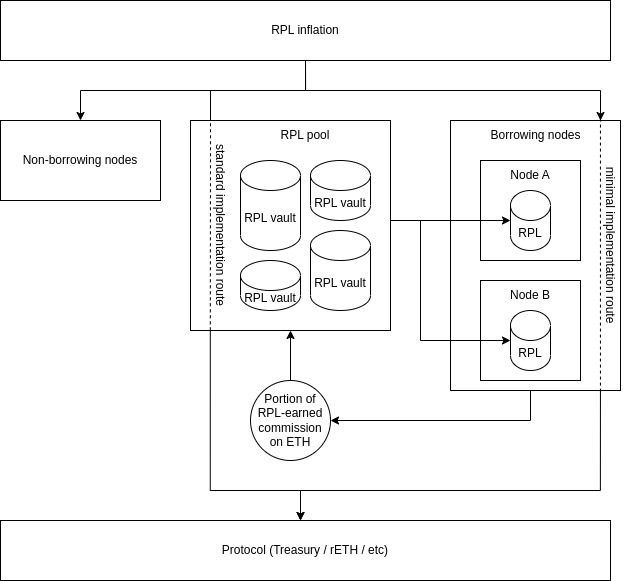

Current tokenomics require node operators to supply RPL to run minipools, and it is known to be a blocker for risk-averse players, thus hindering RP growth. Here I explore one possible way to enrich NO UX by allowing an option to create minipools without the need to invest into RPL token. It is based on a built-in RPL pool that lends RPL to such minipools, captures a portion of inflation and a part of their commission.

Details

Seamless RPL borrowing

Right now operators who don’t want to invest into RPL have an option to borrow RPL from AAVE. A drawback of this option is that it requires more capital as collateral for AAVE, and, an additional to NO duties, management of a loan. To minimize a cost and a friction RP can implement its own RPL pool and a seamless RPL borrowing from it, so that smartnode software manages a loan automatically requiring minimal NO attention.

This can be based on RPIP-31: RPL Withdrawal Address and RPIP-32: Stake ETH on behalf of node.

Implementation

- RP builds its own RPL pool, similar to AAVE’s.

- This pool allows anyone to lock RPL and have a better APR than on AAVE (see Numbers for details).

- This pool gives its participants voting rights, proportional to their share and RPL utilization.

smartnodeshall allow a user to fund a minipool using automatically borrowed RPL from the pool.- This loan does not need a collateral because the system borrows from itself (NO has no access to a borrowed capital).

- In a simplest implementation borrowing minipools cannot be mixed with standard minipools on a single node. Mixing makes collateral calculations harder (per minipool vs per node).

- Minipools funded this way get a share of RPL inflation as normal, but claiming RPL rewards is different:

- Instead of NO RPL rewards are claimed by the pool.

- A portion or all RPL rewards goes to the pool.

- A portion (≥ 0) of RPL rewards can be burned or used in pDAO interests (think of it as a pool fee).

- It is possible to collect a pool fee for funding a protocol owned liquidity, which will allow to reduce a pDAO share of RPL inflation in the future.

- It is possible to set a slightly lower commission for minipools using borrowed RPL in order to increase rETH APR or direct a deducted commission to other places.

- NOs have voting rights only from non-borrowing minipools, because running minipools without owning RPL is not properly aligned with RPL/RP.

Diagram

Loan management

- A loan from the pool has no interest to pay.

- Before a snapshot, if RPL collateral falls below 10% due to price move, either a

smartnodeor one of pool’s smart contracts tops up RPL on borrowing nodes to bring them back to 10%.- If there is not enough RPL in the pool to top up all nodes, it’s not a problem. It means that the pool with utilization over 100% earns less interest, than a maximum possible, hence incentivizing people to supply RPL to bring it back to full capacity.

- Before a snapshot, if RPL collateral exceeds 150%,

smartnodewithdraws excess RPL back to the pool.- This is unlikely to lead to significant loss of gas for transactions because going from 10% to 150% collateral is a rare event.

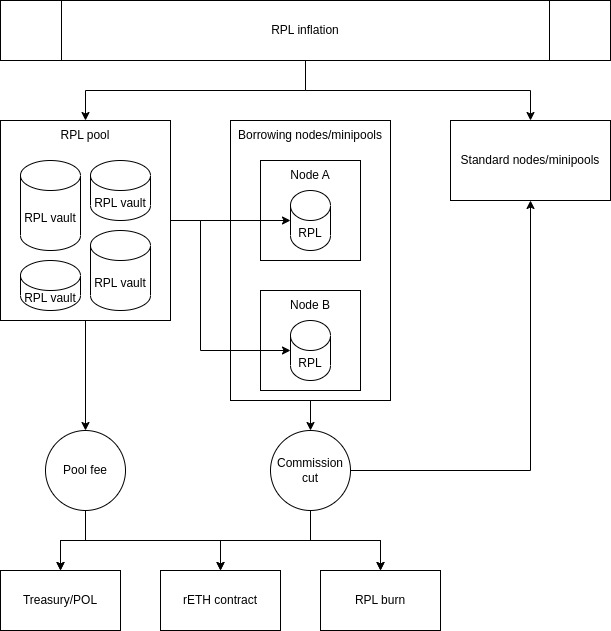

Pool fee and commission cut directions

Options presented here are not mutually exclusive and can be mixed, which allows for a great flexibility for achieving desired outcomes.

Collected fees may be directed to:

1.Treasury / establishing a protocol owned liquidity. This would allow to reduce a pDAO portion of inflation and thus benefits standard NOs bonding their RPL and RPL pool suppliers.

2. rETH contract. This benefits rETH holders primarily.

3. Buying back from a market and sending to null address, i.e., effectively get burned. This benefits all RPL holders.

4. Standard node owners. This makes standard RPL-bonding nodes more appealing.

Numbers

I assume here LEB8 as the only available option for simplicity.

In general a RPL valuation model stays the same as it is now, because all minipools still bond RPL.

Pool possible APR

Inputs:

Current RPL APR = 7.27%.

Current RPL price = 0.014.

Current AAVE utilization = 40% (or 190K of 480K RPL).

Imagine the same demand:

We get 1000 LEB8 funded (190,000 * 0.014 / (24 * 0.10) ~= 1000).

Pool APR is 0.0727 * 0.40 = 2.9% which is twice as high as AAVE average RPL supply APR 1.46%.

Maturity

As we go closer to maturity, RPL price becomes less volatile. Given that RPL APR for standard minipools always outperforms pool RPL APR (at least due to pool fee), it can be expected that a majority of RPL will belong to NOs.

No number here ![]()

Benefits

- Preserves current tokenomics.

- Protocol owned RPL pool allows to borrow RPL without a collateral, thus maximizing capital efficiency for NO seeking to run minipools without investment into RPL.

- Adds an option to run minipools for those who don’t want to invest into RPL token, thus expanding NO base.

- Minimizes friction compared to currently existing option of manual RPL loan from a third party.

- Involves more RP stakeholders into governance.

- Gives RPL more utility by adding another option for RPL yield and governance participation.

Drawbacks

- More smart contracts…

UPD1: Added Maturity section to Numbers.

UPD2: Added revenue stream from commission cut to standard nodes (both diagram and description).