Hey Everyone,

I’m Traver from the Messari Governor team. Since September 2022, Messari has covered Rocket Pool’s governance and its development as a decentralized staking protocol. Messari has also evolved, and part of our growth has included investment in our subgraph and analytics infrastructure.

I partnered with Kentrell Key, a Messari Protocol Services analyst, to compile data that we hope is helpful to the Rocket Pool community as the community aims to align on goals for the rest of 2023.

This post aims to observe rETH’s position as an asset within Ethereum’s greater DeFi ecosystem, emphasizing rETH utilization across layer-2 (L2) and Lending markets.

TL;DR

-

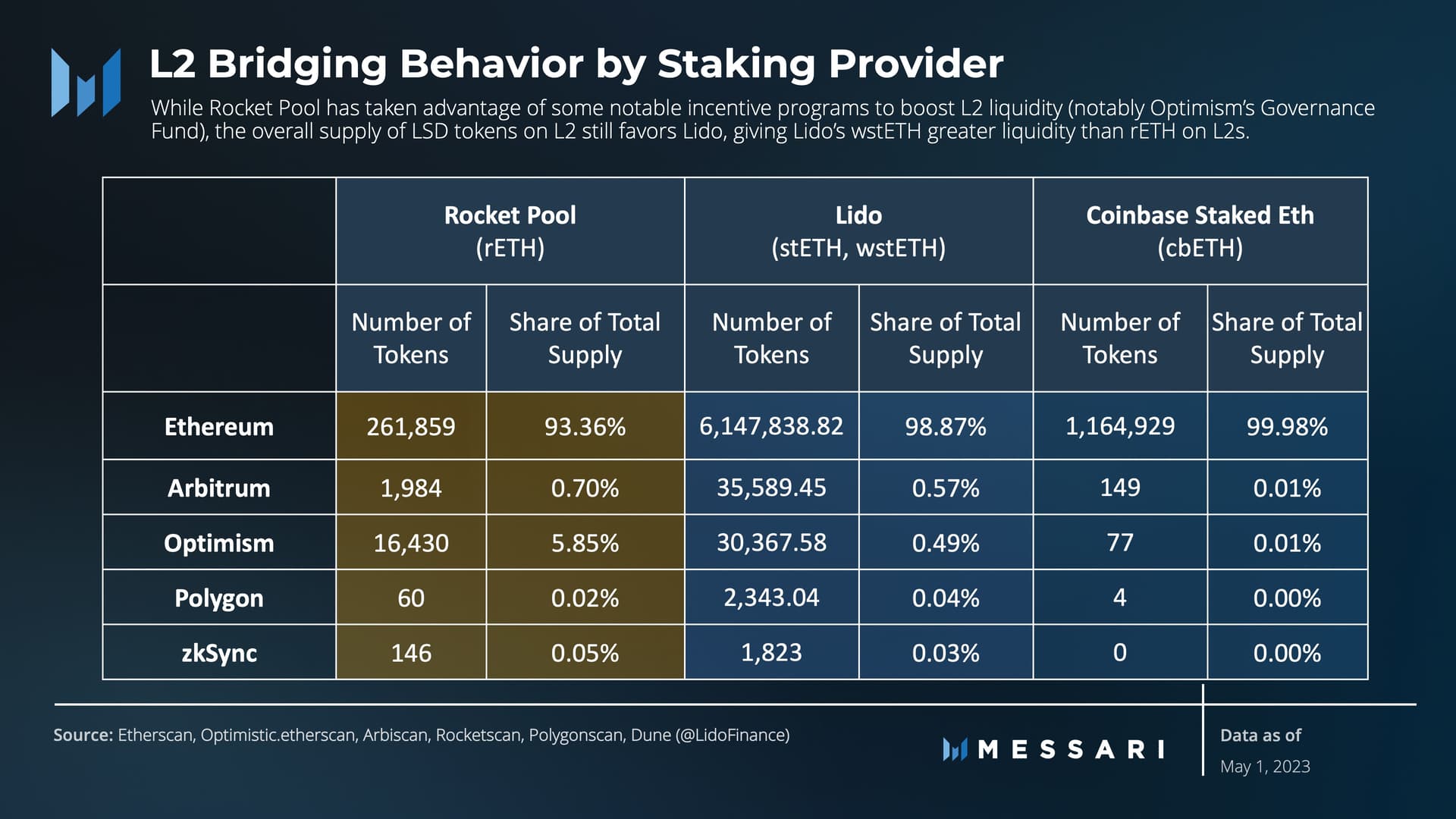

Rocket Pool’s rETH has made significant progress establishing L2 adoption, particularly on Optimism, but lags behind wstETH in terms of overall supply on L2 platforms like Arbitrum.

-

5.85% of the rETH supply and nearly 40% of all rETH holders are on Optimism. This indicates a strong opportunity for Rocket Pool to focus on expanding rETH utilization and growth within the Optimism ecosystem via listings on lending markets like Aave.

-

wstETH’s sheer volume of tokens gives it an advantage in L2 liquidity, and the wstETH lending market on Aave V3 (Arbitrum) has gained significant traction. wstETH has ~18x the supply of rETH on Arbitrum, suggesting that incentives for rETH bridging to Arbitrum and an Aave integration could create a positive flywheel for rETH adoption on L2s.

Layer-2 Liquid Staking Derivative (LSD) Supply Benchmarks

Recent initiatives like the rETH Hop listing and the OP incentive program demonstrate Rocket Pool’s focus on establishing L2 liquidity for rETH. Similar initiatives have led to a higher percentage of rETH’s total supply being bridged to L2s than its competitors. Particularly on Optimism, which holds 5.85% of the total rETH supply and accounts for 37% of all addresses holding rETH, suggesting that retail/smaller holders may prefer to engage with and hold rETH on L2, presumably due to lower transaction costs and fees.

Despite these numbers, wstETH’s sheer volume gives it a distinct advantage in establishing L2 liquidity. Only 0.5% of the total stETH/wstETH supply accounts for nearly twice the amount of rETH on Optimism and around 18x the supply of rETH on Arbitrum. Given rETH’s relatively successful adoption on Optimism, the IMC might prioritize additional incentive strategies for L2 integrations. Despite the relative dominance of wstETH (and, to a lesser extent, cbETH) on Ethereum, these assets have a less defined advantage regarding market dominance on L2.

Layer-2 DeFi

rETH supply on Arbitrum is lagging both rETH growth on Optimism and peer growth on Arbitrum. One key avenue of growth for wstETH on Arbitrum has been Aave lending, where the supply and borrow caps have been raised multiple times.

While rETH is being proposed for Aave on Arbitrum, to date, rETH has significantly fewer bridged assets than wstETH, and if successful, the supply cap for the rETH lending market would be set at 50% of the total rETH supply on Arbitrum, significantly limiting rETH utilization on Arbitrum in its current state. Therefore, incentivizing bridging to Arbitrum could start a flywheel, given the demand for the LSD looping strategy. There is potential for a positive flywheel of more supply leading to higher caps on Aave, driving more demand.

Moreover, Rocket Pool would benefit from proposing a similar listing for rETH on Optimism, where a larger percentage of users holds rETH, allowing for greater utilization of L2 Aave lending markets once rETH is listed.

Lend/Borrow Utilization (Ethereum Mainnet)

Leveraged staking is one of Ethereum Mainnet’s most popular DeFi strategies. As a proxy for utilization, we analyzed how rETH fared against other lending tokens on Aave. Lido’s current market share comfortably exceeds Rocket Pool’s; however, using the percentage of total LSD supply, we wanted to determine how rETH depositors compared to wstETH depositors.

In contrast to the percentage of rETH supply bridging to L2s, a significantly lower percentage of total rETH holders deposit their tokens on Aave. Less than 5% of the total circulating rETH supply is on Aave, nearly a quarter of the same metric for stETH, and just behind cbETH.

Further, rETH depositors have been slower to adopt Aave markets than its competitors. For example, 5% of stETH supply had been deposited by users within 16 days of stETH’s listing on Aave. In contrast, 32 days after rETH was listed, the total share of the rETH supply had only reached 1%. However, following withdrawal enablement and the Atlas Upgrade rETH reached an all-time high of 4.6% of rETH supply deposited on Aave.

One way to incentivize greater adoption of rETH on Ethereum Mainnet might be for Rocket Pool to drive demand by partnering with DeFi yield strategies that build on top of the Aave pool. For example, Messari found that Instadapp, which offers DeFi strategies on top of the Aave Lending market, was the top depositing address of wstETH on Aave V3 and accounted for 44% of historical deposits.

Conclusion

rETH has made great strides in establishing itself as a core DeFi asset over the past year, especially within Optimism’s ecosystem, where it maintains a significant supply share compared to competitors. While Rocket Pool lags behind competitors in total staked ETH, the Atlas upgrade combined with emphasizing DeFi partnerships and integrations could help bolster staker and validator demand.

If the Rocket Pool community is interested in further analysis, we’d be happy to help brainstorm ideas where our analysts and data scientists could help give more value to the Rocket Pool community.