Introduction

Rocket Pool has witnessed remarkable growth since the Shapella upgrade. However, despite the rise in Node Operators (NO), the price of RPL and the quantity of staked RPL tokens have not increased as much as expected. Several factors can influence the price of the RPL token, such as speculation and trader positions, but these are difficult to model and predict.

Abstract

One predictable and measurable source of long-term demand for RPL arises from Node Operators who create pools and post collateral. Our on-chain data analysis shows a decrease in the average collateral ratios despite the transition from 16 ETH minipools to 8 ETH pools. We noticed that the return NOs get on their RPL has become very close to the return generated on their bond. As a result, NOs are incentivized to post the minimum collateral ratio and spin off new minipools instead of holding high collateral ratios or re-collateralizing their existing minipools. Furthermore, our investigation has uncovered a negative correlation between Total Value Locked (TVL) and the demand for RPL. Consequently, this is likely to become more pronounced as the number of minipools grows.

Motivation

Several promising proposals have emerged in the governance forums to address this issue. However, accurately assessing their impact on RPL tokenomics and NO behavior is challenging without the use of multi-agent simulations. To thoroughly evaluate and explore these proposals, we seek funding to develop multi-agent simulations and quantitative analysis tools. These simulations will not only facilitate the assessment of the proposed improvements but also provide a valuable resource for evaluating future protocol changes and community proposals. We are confident that this project has the potential to bring substantial value to the Rocket Pool community.

About Nethermind

Nethermind is a team of world-class builders and researchers. We collaborate with a global developer community and partners to advance the Ethereum, Starknet, and broader blockchain industry. Our work spans Layer 1 and Layer 2 Engineering, Cryptography Research, Infrastructure Management, Smart Contract Security, and Application-Layer Protocol Development.

Blockchain Core Engineering

We are active builders of the Ethereum and Starknet protocols, closely aligning our development and research work with their roadmaps. The Nethermind client supports Gnosis Chain, the OP-stack and Energy Web. Our ecosystem contributions for Starknet include Juno, an open-source full-node implementation, and Voyager, a block explorer and API platform.

Protocol & Enterprise Engineering

We specialize in DeFi, covering DEXs, AMMs, and complex structured products. Our projects include decentralized KYC’d derivatives trading, asset tokenization, and institutional-grade staking. Our engineering teams work closely with clients to create customized Web2 and Web3 software solutions, such as crypto asset analytics, treasury management, trading automation, on-chain wallet monitoring, and token onboarding.

Cryptography, ZK and Protocol Research

Our research team consists of cryptographers, protocol experts, and DeFi researchers, and as such, can tackle complex research challenges. The cryptography team has expertise across a wide range of domains, including cryptographic protocols, zero-knowledge proofs, distributed validator technology (DVT), decentralized identity, verifiable credentials, consensus design, Sybil and white labeling resistance, and oracles. Our protocol research experts are blockchain and financial professionals specializing in DeFi & blockchain protocol research for institutional clients.

Nethermind Security | Smart Contract Auditing, Real-Time Monitoring, and Formal Verification

Nethermind Security is the security arm of Nethermind, providing services related to Smart Contract Audits, Formal Verification, and Real-Time Monitoring. Our work includes Solidity and Cairo smart contract auditing, building protocol-specific custom Forta Network detection bots, and formal verification services across ZK-circuit, EVM-based smart contract, and Starknet smart contract verification.

Specification

- Aim

- Current Tokenomics

- The Impact of the Atlas Upgrade

- Node Operator Profitability

- RPL collateral vs. new Minipools: the NO’s dilemma

- Consequences to RPL Demand

- Collateral at Pool Inception

- Risk Aversion and Collateral Ratio

- The Marginal Return of Recollateralizing

- Game Theory and Collateral Ratios

- Next Steps

Aim

Design and Development of a Multi-Agent Simulation Engine:

Our proposal suggests creating a multi-agent simulation engine to improve decision-making in the governance forum. This simulation engine will model Node Operator collateralization behavior and provide insights into how proposals may impact the network by considering factors like pool numbers and collateral amounts.

Analysis of Selected Proposals:

In collaboration with the Rocket Pool community, we will identify a set of proposal for in-depth examination. Our selection criteria will prioritize proposals with the potential to significantly affect the network, those that are feasible for implementation, and those that align with the community’s overarching vision.

Our deliverables encompass modeling each proposal within the multi-agent simulation framework and generating comprehensive analysis reports complete with recommendations. Throughout this process, we will closely monitor the RPL price, gauge its impact on protocol growth, and identify any potential risks. Additionally, we will conduct parameter tuning to optimize the proposed solutions when applicable.

In the following section, we will outline our approach to creating these simulations and modeling the behavior of NOs in a more precise manner when it comes to posting collateral.

Current Tokenomics

The demand for RPL tokens in the current Rocket Pool tokenomics primarily stems from two sources: 1) Node Operators (NO) who stake RPL collateral, and 2) trading demand from investors speculating on Rocket Pool’s growth.

Trading demand is highly volatile and challenging to predict, especially considering that RPL tokens do not generate income for non-Node Operators. Consequently, the most crucial factor driving RPL tokenomics is the amount of RPL held by Node Operators.

The amount of RPL staked is influenced by two key factors:

- Number of Minipools: The demand for Rocket Pool increases as the number of minipools it manages increases, although we will see later that the relationship is more complex. This factor plays a significant role in driving RPL demand.

- Collateral Ratio: It’s important to note that a higher collateral ratio among Node Operators corresponds to greater demand for RPL. This aspect is particularly crucial as RPL demand could double even if the Total Value Locked (TVL) staked on Rocket Pool remains stable. A mere 1% increase in Node Operators’ collateral ratio would result in a demand for approximately 374K RPL tokens, based on 11th August 2023 prices. Remarkably, this represents 1.9% of the current supply.

In terms of supply, RPL tokens are generated through an annual inflation rate of 5%, which is split among Node Operators, the oracle DAO, and the protocol DAO.

One challenge with the current tokenomics is that NOs lack strong incentives to maintain a high level of collateral. If their collateral falls below 10% of the borrowed amount, they will lose their RPL rewards. However, as we will explore further, losing RPL rewards doesn’t significantly impact the profitability of NOs and may even be advantageous in terms of risk-adjusted returns.

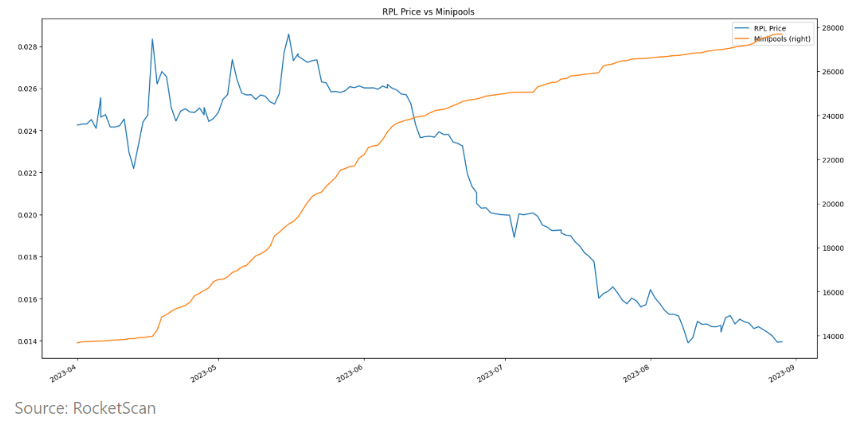

Therefore, this partly explains why, despite the surge in minipools after the Shapella Upgrade, the RPL/ETH token price experienced a significant decline.

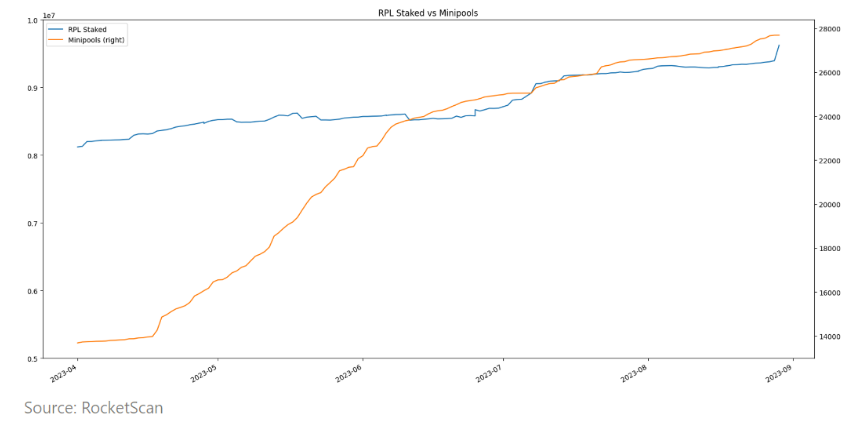

Since Shapella, the number of RPL staked only increased by 20%, while the number of minipools doubled. As we can see, the link between TVL growth and RPL demand is not straightforward, and that is something that should be corrected.

The Impact of the Atlas Upgrade

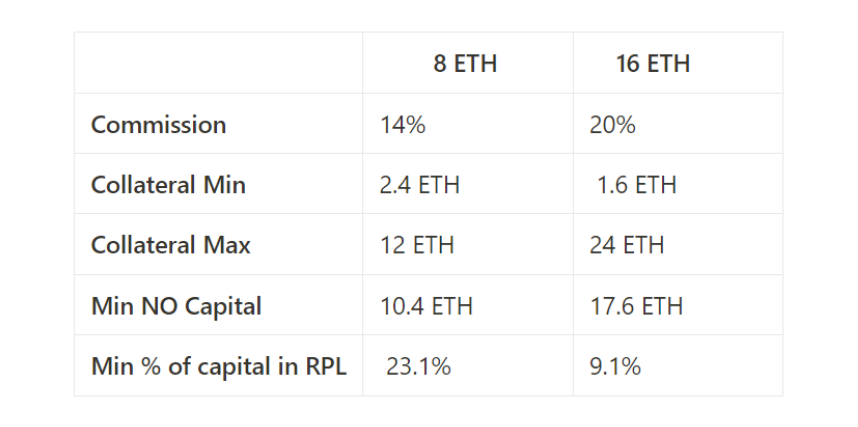

The Atlas Upgrade has enabled the creation of 8 ETH minipools. Below is a comparison table between 8 ETH and 16 ETH minipools. The new upgrade enables higher leverage for network operators (NO), which offsets the lower commission rate. However, more leverage means more risk for NOs, as a larger part of their capital is now tied up in RPL tokens, increasing from 9.1% to 23.1%. This makes them more exposed to fluctuations in RPL price and makes the protocol more prone to sudden withdrawals.

Node Operator Profitability

Let’s examine the profitability of minipools, which can be attributed to two primary sources:

- ETH staking

This component consists of the complete staking return earned by the Node Operator (NO) on their bond, without any commission deductions, as well as the commission the NO receives on their borrowed stake.

- RPL incentives

We can therefore determine :

- ETH ROI (Return Over Investment): yield NO get on the ETH they provide. That is the staking income divided by the size of their bond.

- RPL ROI: return NO get on the RPL they provide. It can be defined as {RPL income/ RPL staked).

The return on investment (ROI) for Ethereum (ETH) depends solely on the staking yield, leverage (i.e., the size of the bond), and commission rate. On the other hand, the ROI for Rocket Pool (RPL) has a different dynamic since the inflation rate and percentage of printed tokens given to Node Operators are fixed. With the introduction of new minipools, there is an increase in the proportion of RPL tokens being staked, resulting in a decline in RPL ROI. This diminishing ROI makes it less appealing for NO to allocate collateral as the protocol expands. Consequently, this situation heightens the security risk associated with the protocol.

RPL collateral vs. new Minipools: the NO’s dilemma

As highlighted above, NOs must consistently choose between increasing their RPL collateral (and their RPL rewards) and creating new pools. So, let’s try to understand what would drive them to choose one versus another.

ETH ROI

Staking yields can be volatile daily due to MEV opportunities but we could assume average annualized rates of 5%. This means that in an 8 ETH minipool, a NO can expect to generate a 7.1% ROI on their investments. Worth noting that the system is very advantageous for NOs as they can expect to increase their returns by 42%.

RPL ROI

The RPL returns are more variable because in order to benefit from RPL rewards, NOs need to maintain a minimum collateral ratio of 10%. Additionally, 3.75% of the annual RPL inflation is distributed directly to all NOs who have staked the required amount of tokens.

Optimizing NOs returns

Financial theory tells us that RPL returns need to compensate NOs for the potential loss of capital and token volatility. As a result, one would expect higher RPL returns. From a NO perspective, the return on their ETH ROI can be considered as a risk free rate. Their target RPL ROI can be expressed as follows:

Consequences to RPL Demand

These circumstances have significant implications for RPL demand and the overall tokenomics. Notably, RPL exhibits high volatility compared to ETH. Analysis of historical data from the year leading up to 13 August 2023 reveals an annualized volatility of 76.5% for the RPL/ETH pair. In comparison, the long-term Sharpe Ratio for bonds and equities typically falls within the 0.1-0.3 range, suggesting that the desired target returns for RPL should range between 15% and 30%.

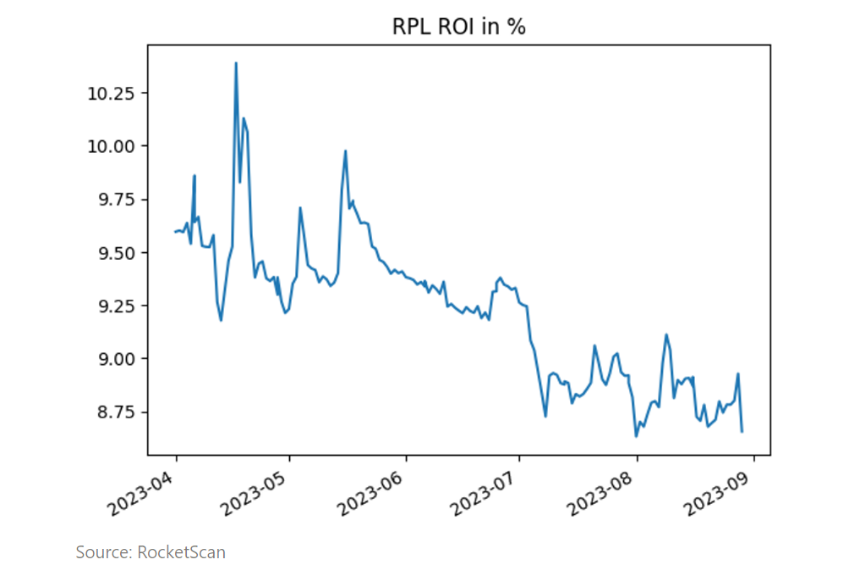

Since Shapella, the RPL ROI has been lower than the ideal target and has been relatively stable. It seems that NOs are not willing to accept ROIs significantly below 9%.

RPL ROI is inversely proportional to the percentage of RPL staked and indirectly to the number of minipools. As the protocol develops, it becomes unprofitable for Node Operators to hold extra RPL collateral. The behavior of a NO can be modeled as follows: when a NO creates a minipool, they would usually put the minimum required RPL if the RPL return is too low. Some NOs might be tempted to include a buffer so they do not have to consistently monitor their collateralization and be sure to be eligible for rewards.

Game Theory and Collateral Ratios

The existing tokenomics appear to overlook the game theory dynamics between NOs and their adjustments to collateral ratios. We consider this aspect crucial and will outline our approach to modeling these interactions in multi-agent simulations.

Collateral at Pool Inception

The behavior of a NO can be modeled as follows: when a NO creates a minipool, they would usually put the minimum required RPL if the RPL return is too low. Some NOs might be tempted to include a buffer so they do not have to consistently monitor their collateralization and be sure to be eligible for rewards.

Risk Aversion and Collateral Ratio

The collateral ratio within the Rocket Pool system is subject to fluctuations based on the price movement of RPL. If the value of RPL depreciates relative to ETH, the collateral ratio decreases, resulting in Node Operators (NOs) incurring mark-to-market losses. Users with higher collateral ratios are more significantly affected by these fluctuations. For instance, NOs of 8ETH minipools have approximately 23% of their capital tied up in RPL, meaning that a 10% decrease in RPL price would lead to a capital loss of 2.3%.

When the collateral ratio falls below 10%, NOs may hesitate to purchase additional RPL tokens (i.e., double down) to obtain RPL rewards since doing so could expose them to further losses. In a market characterized by high volatility and a low-risk appetite, this situation fails to provide the stability mechanism that the protocol initially sought to achieve.

The collateral ratio will fluctuate with the RPL price. If RPL depreciates vs. ETH, the collateral ratio drops, and the NO takes a mark-to-market loss. Users with higher collateral ratios are more impacted. As we have seen before, NOs of the 8ETH minipools have at least 23% of their capital tied in, so a 10% drop in RPL translates to a capital loss of 2.3%.

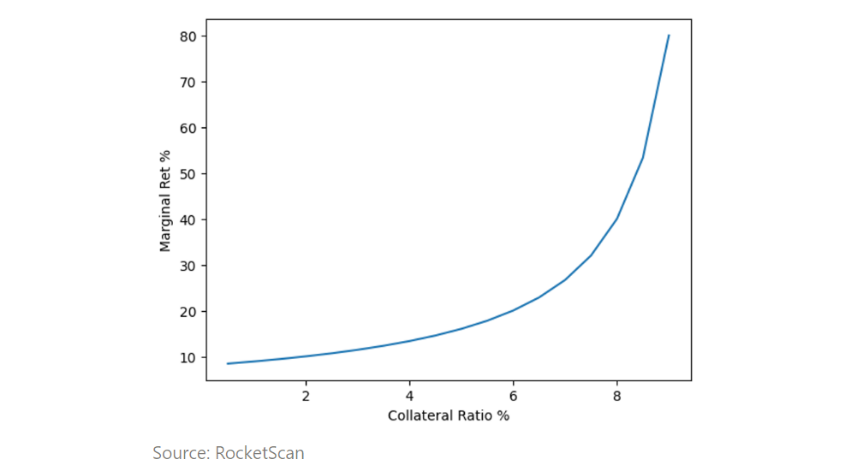

The Marginal Return of Re-collateralizing

Let’s consider an example where you, as a Node Operator (NO), have a collateral ratio of 8%. In this scenario, you have two options:

- Do nothing and forego RPL rewards: By maintaining the current collateral ratio, you would not be eligible to receive RPL rewards.

- Add 2% of RPL to meet the minimum collateral threshold: If you choose to add 2% of RPL to your collateral, you will meet the minimum requirement and become eligible for RPL returns. The marginal impact of adding this additional RPL is significant. The marginal return can be calculated as the total RPL rewards divided by the 2% increase in collateral. Specifically, you would receive a return of 10% * RPL_ROI / 2%, resulting in a marginal return 5 times the original RPL ROI.

The marginal return from re-collateralizing could be generalized as:

So, as long as the collateral ratio is not too low, it makes sense for RPL NOs who believe in the protocol to re-collateralize. However, if losses are too high, they might throw out the towel and stop recollateralizing. As a result, it is important to incorporate a stop loss in our simulations.

If the collateral ratio drops below 7%, based on current RPL ROI, the marginal return drops below 30%, making it less attractive for NOs to re-collateralize.

Next Steps

-

We would appreciate community feedback regarding our report.

-

Depending on the community’s appetite, we will apply for a grant from the DAO via the next grant round to achieve the objectives seen below.

-

Design and Development of a Multi-Agent Simulation Engine:

- We propose building a multi-agent simulation engine to enhance the decision-making process within the governance forum.

- The simulation engine will incorporate the collateralization behavior of Node Operators, providing valuable insights into the impact of various proposals on the network.

- This engine will measure key factors such as the number of pools, the amount of collateral, and other relevant metrics.

- Deliverable: We will ensure the code repository for the simulation engine, with its documentation, is made available to the Rocket Pool community, enabling further development and refinement.

- Time to deliver: 2 months

-

Analysis of Selected Proposals:

- As a collaborative effort, we will work closely with the Rocket Pool community to identify and incorporate a few selected proposals we would like to examine.

- These proposals will be chosen based on their potential impact on the network, feasibility, and alignment with the community’s vision.

- Deliverable: We plan to model each proposal in the multi-agent simulation framework and produce an in-depth analysis report with recommendations. We will track the RPL price, its impact on protocol growth, and identify potential risks. When relevant, we will run parameter tuning to optimize the proposal.

- Time to deliver: 2 - 4 weeks per proposal, depending on the level of complexity.