The ratio is really kicking our butt - we’re burning reserves and would have about half a year of runway with no pDAO action and constant ratio

We’ve adopted a loose framework of “1.25 ETH/fortnight for up and coming L2s” - no particular schedule here, but we expect to add more over time.

If you have opinions here, we’d love to hear from the community. We struggled a couple of times on frameworks for deciding how much to give to different L2s. Part of the current thought is “for now, let’s give up-and-comers a smallish amount so we’re present early, and we can figure out where we go later”.

One more question for the community – the IMC has been providing an ETH-denominated amount of incentives for rETH/ETH liquidity and a split ETH/RPL-denominated amount of incentives for RPL/ETH liquidity. This is nice for liquidity because it essentially smoothes RPL price volatility away.

Do you think we should be reducing those numbers some as RPL ratio has gotten hit? This could be partial, of course. Or should we stick to the smooth choice?

IMC has been talking about this a bit internally and we are looking for community feedback on this rough plan:

We will aim to maintain one year of runway (13 periods) in the IMC treasury. This attempts to strike a balance between smoothing out ratio volatility and keeping the IMC solvent.

We will count POL beyond “minimum safety” as part of runway.

For next period we are looking at keeping everything but Aura as is and reduce Aura accordingly, because bribe efficiency there has been going down.

Going forward we will reevalute and reduce spend further as necessary to maintain the one year runway.

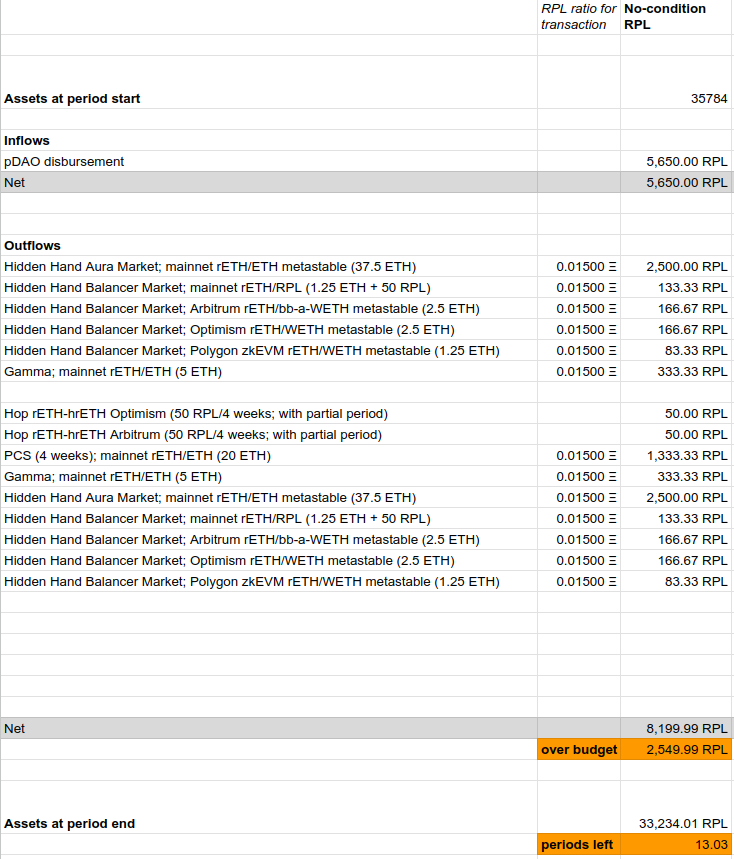

Assuming a 0.015 ratio, this would roughly translate to lowering Aura from 53 ETH to 37.5 ETH for Budget 14 (September 1 - September 28):

If you have opinions here, we’d love to hear from the community. We struggled a couple of times on frameworks for deciding how much to give to different L2s. Part of the current thought is “for now, let’s give up-and-comers a smallish amount so we’re present early, and we can figure out where we go later”.

If you have opinions here, we’d love to hear from the community. We struggled a couple of times on frameworks for deciding how much to give to different L2s. Part of the current thought is “for now, let’s give up-and-comers a smallish amount so we’re present early, and we can figure out where we go later”.