Gov Stuff

I’ve generated a rewards tree using the proposed formula for target interval 15 which ended a day ago. Attached you’ll find the tree, along with a csv showing how each node’s rewards would have been different if this proposal had been enacted before interval 15.

Click here for the rewards tree

Click here for CSV summary

Once downloaded, you can search the CSV for your node id to find your personal impact. You’ll need to lowercase your node id first.

For example:

| node |

interval15rewards |

proposed |

factor |

delta |

| 0x18845fd4aa047d6d43c934cc37aca94f85def683 |

25.0122713590862 |

21.3127893045889 |

0.852093318460127 |

-3.69948205449725 |

This is my node. In interval 15 I received 25 RPL of rewards. This proposal would reduce that to 85%, or 21.3 RPL, which is a difference of -3.7.

On the balance, I’m in favor of measures to make inflation impel growth, so I’m leaning in favor. However, I’m sensitive to the notion that some people may feel rugged.

| node |

interval15rewards |

proposed |

factor |

delta |

| 0x17fa597cec16ab63a7ca00fb351eb4b29ffa6f46 |

6023.22623367632 |

3373.75553590557 |

0.560124326236104 |

-2649.47069777075 |

| 0xca317a4eccbe0dd5832de2a7407e3c03f88b2cdd |

2142.75795001593 |

974.570809890287 |

0.454820764931962 |

-1168.18714012564 |

| 0x895f6558f0b02f95f48ef0d580ec885056dcccc6 |

1808.81809820746 |

778.456936814446 |

0.43036772884233 |

-1030.36116139301 |

| 0x7c5d0950584f961f5c1054c88a71b01207bf9cb7 |

1808.81809820746 |

778.456936814446 |

0.43036772884233 |

-1030.36116139301 |

| 0xacb7cfb56d6835d9e2fa3e3f273a0450468082d9 |

1808.81809820746 |

778.456936814446 |

0.43036772884233 |

-1030.36116139301 |

| 0x663cbbd93b5ee095ac8386c2a301eb1c47d73aa9 |

1808.81809820746 |

778.456936814446 |

0.43036772884233 |

-1030.36116139301 |

| 0x22ffba127f6741a619fa145516ef4d94b90f093a |

1417.00027016498 |

406.753997115619 |

0.287052871957646 |

-1010.24627304936 |

| 0xb8ed9ea221bf33d37360a76ddd52ba7b1e66aa5c |

1549.03842573998 |

765.819471099213 |

0.494383779236064 |

-783.218954640764 |

These are the biggest losers by total swing. It’s a mix of whales whose support the protocol has benefited from. They can mitigate their losses substantially by migrating to leb8s, but I would like to hear from them to understand why they haven’t already done so, and in general to get their opinions.

At the top we have @thomasg followed by an anon, then patricio and marko’s nodes, and some more anons.

| node |

interval15rewards |

proposed |

factor |

delta |

| 0x2fc184459069dc780b478f7e3c9ffd79e40842a3 |

449.767509478073 |

770.649998412312 |

1.71344079368161 |

320.882488934239 |

| 0xfd0166b400ead071590f949c6760d1ccc1afc967 |

371.75691749514 |

677.058729081032 |

1.82124043216999 |

305.301811585892 |

| 0xd91eecc267ff626399798040d88de62c9e70acf0 |

359.930169559552 |

655.519377559656 |

1.82124043216999 |

295.589208000104 |

| 0x84ba027280cc6cc1e592a01270c5f21a494f46cb |

291.487883004815 |

530.869518016004 |

1.82124043216999 |

239.381635011189 |

| 0xacfad9f0d80f74ad7e280a55ea025f4f09844b0f |

271.330533561145 |

494.158138203814 |

1.82124043216999 |

222.827604642669 |

These are the five biggest winners. Unsurprisingly, they have leb8s and are closer to their borrow limits. Interestingly (for me, anyway), 0xfd0166b400ead071590f949c6760d1ccc1afc967 - click here reprises his role as a governance subject. See my last post about him - click here.

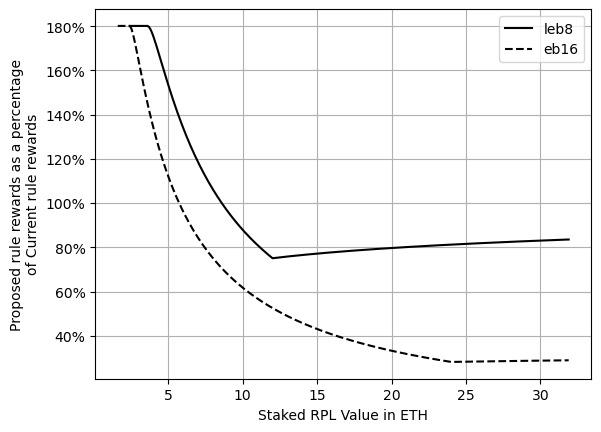

Not that the impetus to exit to stay above 10% is a function of the rewards power curve, but I do worry this change will reinforce that behavior. 0xfd01 has exited over a third of their minipools to stay above the 10% collateral threshold, which has kept them in the “sweet spot” on the proposed curve to maximise their rewards. I wonder if there shouldn’t be a mechanism that ramps the rewards power up after 10% creating a local maximum at the collateral rate we consider to be an optimal balance between security and capacity before decaying. As it stands, with this proposal, a node operator skating by at 10.00% will be in a position we have financially defined as borderline undercollateralized, but still receiving the maximum rewards power.

That’s all for my ambling.

Tech Stuff - skip this. please.

Methodology - click here

This proposal includes a ln(), which, obviously, is feasible. The problem comes in the standardization. Treegen is primarily a specification. Specifying integer math was fairly straight forward- you say that the integer container size is unbounded, you specify the order of operations, and everyone gets the same result.

ln() presents more of a challenge, and will likely need to be approximated. Because floats are stored in a representation of s(2^x)*y, a log2() transformation may actually be easier to specify. However, for ease of implementation, I’d suggest what Val originally suggested to me when I complained about this: a LUT which approximates the desired curve.

The curve is actually 3 dimensional, so the simplest LUT would be one that takes a decimal value for staked_rpl_value_in_eth / borrowed_eth (ie where the number of sigfigs is preordained, see below) and simply returns the weight. We can set a reasonable upper bound on the input (because nobody is likely to care about rewards growth above, say, a quotient of 20). The LUT itself will likely need to be generated not by hand but by machine and stored in a way where implementors can trivially convert it to a compile-time constant value in the language of their choice, well-optimized for interval queries.

A interval tree - click here comes to mind, but there’s more efficient options: We can quantize the inputs- That is, say your input to the function to 3 sigfigs is 0.789, but we quantize to 2, 0.79, and the LUT has fidelity to 2 sigfigs. In this case a simple array provides O(1) lookups, an improvement over a tree’s O(logn) complexity.

And that’s all for my rambling!

Edit: Any of the people I called out as wanting to hear their opinions (thomas, etc), I can make myself available to do more analysis and discuss. Happy to rerun treegen for hypothetical scenarios (eg, what happens if you migrate to leb8s, or exit N minipools, etc)