Dear RP community,

The team at 1kx appreciates the community’s enthusiasm for enhancing Rocket Pool’s tokenomics and recognizes the significant efforts behind the current tokenomics proposal. We would like to suggest a slightly different approach, viewing our proposal not as a replacement but as an extension of the existing one.

Given the timelines involved, we have attempted to strike a balance between getting the proposal in front of the community as soon as possible, while also providing sufficient detail to allow for an informed comparison.

In brief, our primary disagreement with the existing rework proposal is that it prematurely abandons RPL’s primary value driver—the RPL collateral requirement for validators. We recognize that the proposed token rework contains other benefits, but we believe Houston’s new features can be better leveraged to further accelerate our main goal of maximizing rETH’s sustainable yield to position Rocket Pool as the most attractive LST in the space – we call this the “maxETH” strategy.

Introduction: “maxETH” <3 rETH

One main reason Rocket Pool has become so popular is because of its alignment with Ethereum’s core values. However, this merited gravitation towards decentralization can only attract so much TVL, and the average user’s preferences are driven by three realities: high yields, deep liquidity, and DeFi utility. Since we believe that the former leads to the latter two, our primary goal is to maximize the rETH’s sustainable APY as it is the single most important attribute for any LST.

The “maxETH” strategy has 3 main components:

- Align rETH growth with NO growth by adding a dynamic global commission structure based on deposit pool utilization

- Introduce RPL delegation to provide additional utility to RPL and allow stakers to select highly performant NOs from a Node Operator Performance Dashboard

- Safely accelerate protocol growth and reduce MEV theft risk by accelerating Bonding Curves adoption

Proposed Changes in Brief

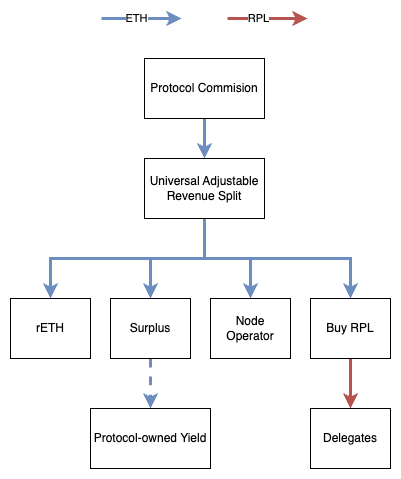

The core of our proposal is a delegated staking system, described in more detail below.

We propose to initially set the surplus_share to zero, increasing rETH APY.

1. Dynamic Global Commission

Capital in the deposit pool is idle and does not contribute to rETH APY. When the deposit pool is full, 18k of that ETH is not earning rewards, dragging down the average APY. Thus, aiming for maximum capital utilization —an empty deposit pool—is doubly important for rETH APY.

The protocol previously operated a dynamic commission rate that was set at the time of creation and applied for the lifetime of the validator. However, this approach led to gamification, as operators would skip a few days of rewards and wait for the deposit queue to fill up to lock in a 20% lifetime commission rate.

This had a negative impact on rETH’s growth and APY. There was slower growth due to NO waiting games and lower overall rETH APY due to overcompensation to NOs.

While gameable, this mechanism elegantly tied NO incentives to the protocol’s growth requirements, increasing rewards when necessary to attract new NOs.

We propose a new implementation of the dynamic commission with one important change: the variable commission rate applies to all validators regardless of the prevailing rate at the time of initialization.

This helps maximize rETH APY in two ways:

- The protocol pays a higher commission only for as long as is necessary to attract new NOs

- An individual NO has less incentive to wait for the higher commission rate

The prevailing commission rate would be set by a contract function. The function would calculate the desired position on the commission curve based on the available capacity of the deposit pool. We envision this function being executed by the oDAO, although it would be executable by anyone so long as there was sufficient time between invocations.

The rate change function would be similar to that of a DeFi lending pool, where the commission would spike if the deposit pool hit a certain size. Some illustrative values are:

| Deposit Pool Utilization | Commission Rate | NO’s share | Staker’s share |

|---|---|---|---|

| 10% | 5.9% | 1.18% | 4.72% |

| 50% | 9.5% | 1.9% | 7.6% |

| 80% | 12.2% | 2.44% | 9.76% |

For those who want a deeper explanation, the dynamic commission rate on ETH staking rewards grows linearly with the deposit pool size and can be parametrized as follows:

d is the current deposit pool size in ETH, d_min and d_max the minimum/maximum values of those we consider (proposal: d_min=0 and d_max=18k) and c(d) the commission rate which is capped at c_max (proposal: 14%) and c_min (proposal: 5%).

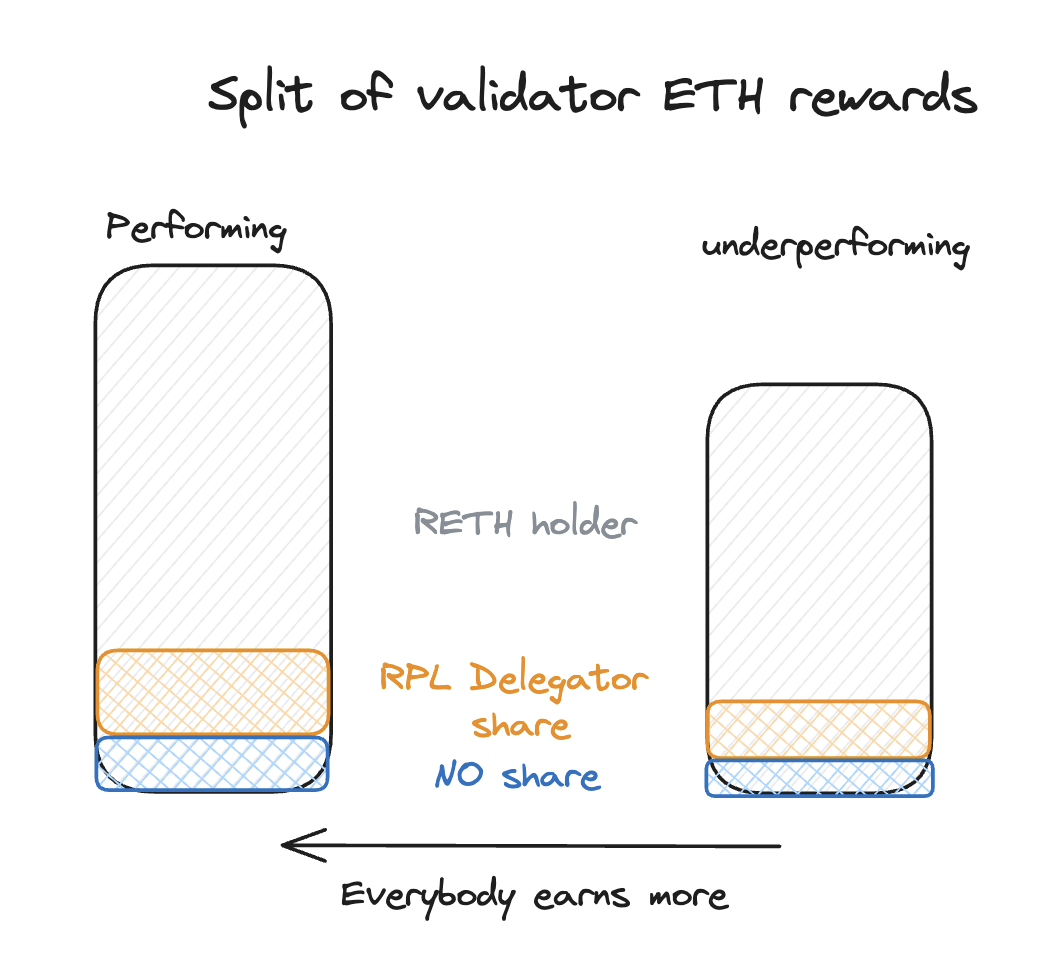

This overall commission rate is split between i) the node operators (NO commission), ii) the RPL stakers or more specifically delegators (stake commission) and iii) a protocol share (surplus share). The motivation is similar to the ones outlined in the initial community proposal, yet we suggest a different dynamic:

i) The node operator commission share is initially a flat share of the overall commission rate and increases at a given kink point (k) of the deposit pool size, similar to a DeFi lending pool:

The node operator hence receives s_NO(d)*c(d) as commission from the ETH staking rewards. We propose a minimum share of 20%, a maximum of 70% and the kink at 80% if the maximum deposit pool size is reached (i.e. 14.4k ETH).

ii) The stake commission share is the share of ETH rewards that gets swapped to RPL and paid out to stakers that are delegated to node operators. We propose that the initial stake commission rate equals the total commission minus the node operator commission (see i). See next for our rationale.

iii) The protocol surplus share: we propose to leave this share at 0 for now for two main reasons: first, we want to maximize rETH yield by lowering the overall commission rate. Second, as mentioned in our previous forum reply, the protocol’s current TVL is not high enough to justify any sort of value capture. If Rocket Pool were to use the surplus share, we have a recommendation that we reference in point #6.

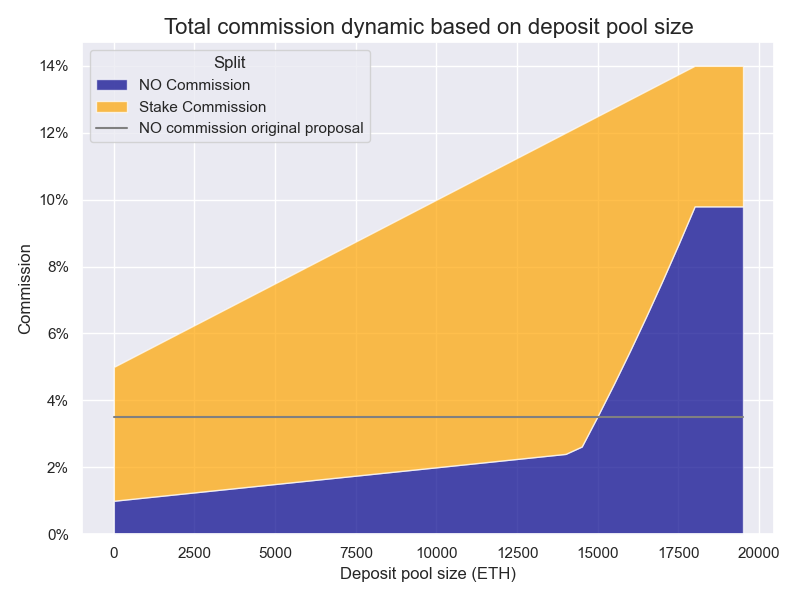

With that, the proposed commission share and its distribution is as follows:

The node operator commission share we propose (20-70%, blue area) is, on average, 3.2% when considering all deposit pool sizes, which is only slightly lower than the initially suggested 3.5% figure, as shown by the gray line. If the deposit pool is empty, the total commission will equate to ~5%, which boosts rETH’s APY by a notable 10% compared to the current product. A theoretically empty deposit pool would allow rETH to surpass stETH’s yield by a full 15 bps, which massively incentivizes more TVL for Rocket Pool. If the deposit pool is full, we’re temporarily over-incentivizing NOs to spin up new validators with higher commissions, ensuring our overall protocol efficiency stays high. This mechanism is a very powerful feedback loop that can lead to sustainable TVL growth.

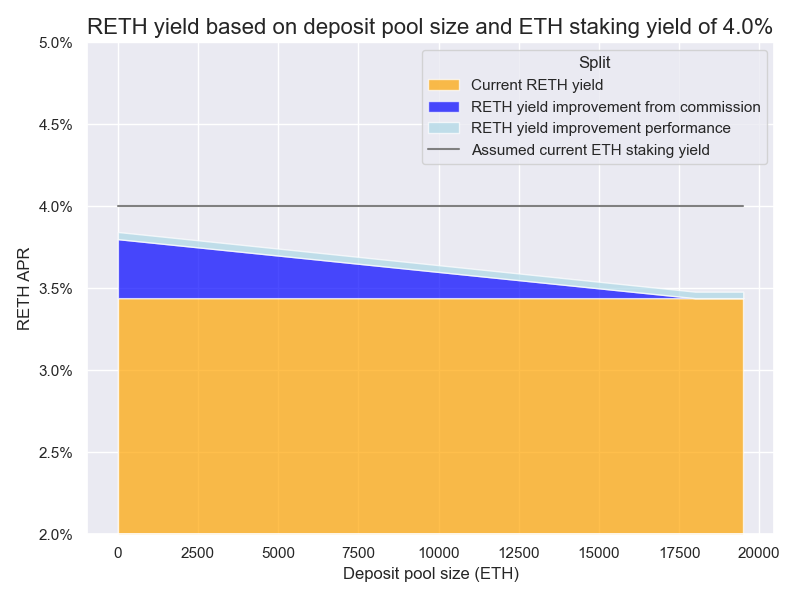

Combined with some assumption of gains for performance in general based on the research by ArtDemocraft, we could see rETH’s yield pass stETH over the long run, or at the very least a significant reduction in the current yield gap between stETH and rETH. This would make rETH one of the best-yielding LSTs:

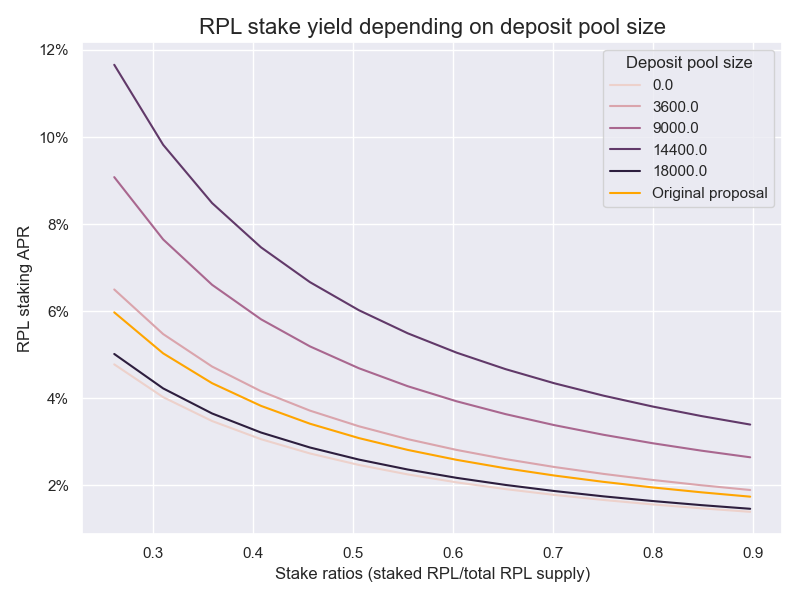

For RPL stakers, the actual APY depends largely on the total amount of RPL staked and the price of RPL in terms of ETH. We fund the RPL staking rewards by purchasing RPL with earned ETH staking reward commissions. Thus, if the RPL price increases vs. ETH, then the RPL staking yield decreases and vice versa. This is true for the original proposal as well. Hence, the following assumes the current price relation of RPL and ETH. If the proposed minimum of 150 RPL per validator is staked, we end up with about 25% of the total RPL staked and consequently the highest yield. The peak income for stakers is at the kink of our commission split between node operators and stakers at 14.4k ETH in the deposit pool (see chart above). At that level and minimum stake ratio, stakers would earn over 10% APR:

This is almost double the yield for stakers compared to the original proposal, represented by the orange line. Please click here for more simulation data and associated assumptions above.

This change would introduce the following protocol parameters:

| min_commission | Minimum commission rate |

|---|---|

| max_commission | Maximum commission rate |

| commission_change_min_interval | Minimum time that must pass between changes to commission rate, in seconds. |

| commision_relative_step | Maximum amount that commission can be changed per update, expressed as a percentage of current rate |

The introduction of a dynamic global commission will contribute towards the maxETH initiative by minimizing protocol value capture, optimizing for node operator and staker payouts at varying deposit pool sizes, and prioritizing rETH yield payouts at all times.

2. RPL Delegation

Key to our proposal is the introduction of delegated staking.

Houston introduced the concept of “whale marriages”, whereby one party can provide the RPL while another provides the ETH. This has previously been possible through the use of splitter contracts but technical complexity and poor UX led to limited uptake.

Like many in the ecosystem, we believe this is of paramount importance to unlocking NO growth as it allows the protocol to onboard NOs who do not want to take on RPL exposure.

We propose to introduce delegated staking, effectively a matchmaker for “whale marriages”. This provides a Schelling point where NOs can compete to attract delegators, and RPL delegators can make informed decisions about their delegations.

The goal is to eliminate the friction of pairing these counterparties, unlocking the full potential of Houston.

Should our proposal pass, we would follow up with a future proposal to integrate the existing penalty research into the delegation system, further increasing the incentive for NOs to perform and for delegators to choose performant NOs. This involves making NOs (and their delegators) liable for the cost of poor performance, ensuring the rETH APY approaches its theoretical maximum.

To mitigate centralization risk a per-NO delegation cap would be applied, preventing any single NO from accumulating too much voting power (e.g. a cap of 1% would ensure that no single NO could have more than 1% of RPL supply delegated to them).

In the future, we could also introduce the idea of separating reward delegation from voting delegation. An RPL staker could receive rewards from the NO that provides the highest yield, while still delegating their voting power to a community member who supports their ideals.

Improving Performance

Among notable ETH staking protocols, Rocket Pool currently has the lowest performance on Rated Network, falling behind players such as Swell, EtherFi, Ankr, Lido, Stader, and Stakewise. While each missed attestation is relatively small, the aggregate effect of the missed attestations drags down rETH’s APY.

We believe this can be corrected with a market design that incentivizes delegation to operators with strong performance, which in turn can reduce missed rewards and help increase rETH APY. Based on the assumptions in ArtDemocraft’s research, we could optimistically expect to see a potential APY increase of up to 0.07% simply due to performance improvements amongst the largest struggling NOs.

To do this, we need to introduce a forcing function that encourages NOs to improve performance. The best way to do this is to create a direct link between performance and rewards.

As part of our proposal, a portion of the NO’s rewards will be shared with their delegators. The higher the NOs rewards (i.e. the fewer missed attestations), the more rewards received by their delegators. The more delegators an NO has, the more collateral they have for launching additional validators. Thus we introduce a positive feedback loop where operators with the best performance will likely attract more rewards. This introduces competition between NOs to miss the fewest attestations, which will increase the total amount of rewards, which will increase rETH’s APY.

To allow RPL holders to make informed decisions when choosing delegates, we will introduce a Node Operator Performance Dashboard (NOPD). This will be built on publicly available data so we might see multiple NOPDs deployed by different parties.

The variable nature of MEV makes it challenging to compare validator earnings side by side. We, therefore, propose making participation in the smoothing pool mandatory for those opting into delegation, reducing the inherent variability in rewards.

Democratizing Whale Marriages

Under the current system, Whale Marriages have some centralization risk, benefiting large RPL holders who can strike deals with node operators at scale. Our delegation system democratizes the process of providing RPL for delegation and gives smaller RPL holders just as much chance to take part as larger holders.

It would be a lot of work for a polygamous NO to individually coordinate with 10,000 delegators providing 10 RPL each. This gives an advantage to the whale with 100k RPL, who would find it easier to match with a “marriage partner.” We believe that larger holders should not have an unfair advantage merely because they have more capital, and leveling the playing field provides more support for the Charter goal of prioritizing decentralization.

By removing the friction of matching RPL and ETH counterparties through a simple dashboard, we can rapidly accelerate the rate at which ETH can be deployed, further accelerating rETH’s APY growth.

Reducing Risk of MEV-theft

In addition to the above benefits, implementing delegation allows us to further reduce both the probability and impact of MEV theft. Delegated RPL provides additional capital which can be slashed to a) punish NOs, and b) make the protocol whole after MEV theft.

As noted in the Bond Curves RPIP, the current proposal does not fully protect against MEV theft. While the nature of MEV makes it challenging to achieve full protection, we believe we can improve upon the current proposal.

In the current proposal, if a NO with a single 8 ETH minipool steals 20 ETH of MEV, rETH APY is lower than it should be.

As part of the delegation system, delegators will stake their RPL against a NO’s megapool contract. This provides additional capital which can be used to slash NOs who steal MEV. This has three benefits:

- The cost of MEV theft is increased, making it less likely to occur

- If MEV theft does occur, the protocol has a higher chance of recovering the stolen funds

- We do not need to force-exit the NO in order to recover the capital - we can immediately slash the staked RPL (and still force-exit the NO if more collateral is required, and might wish to do so as punishment)

RPIP-42 notes that:

> “We willingly take on somewhat more MEV-theft risk for the smallest NOs”

Our proposal allows the smallest NOs to attract delegated RPL, strengthening the anti-MEV-theft provisions. Thus, we provide further support for this goal without taking on additional MEV theft risk.

With additional RPL collateral available for slashing misbehaving or poorly performing NOs, and sufficient buy-side demand for RPL, we believe the Bond Curves (RPIP-42) work could potentially be safely accelerated.

Delegation Parameters

The incentive to delegate RPL to the top-performing operators maintains RPL’s core utility and enhances the protocol’s overall validator rewards. This, in turn, leads to higher rETH yields, advancing the maxETH initiative.

3. Updates to RPIP-42: Bond Curve Proposal

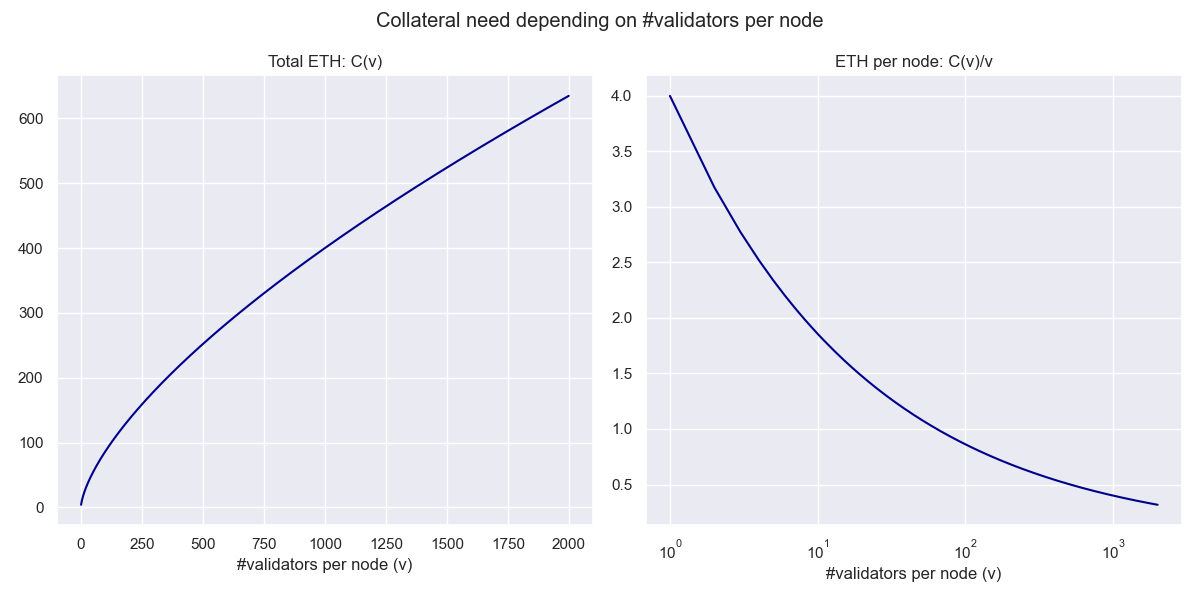

Currently, node operators need to put up a set amount of ETH per validator (e.g. 8 ETH collateral, 24 ETH borrowed) when launching validators. Also as suggested within RPIP-42, there is general alignment within the community that from a risk/reward perspective, lower amounts of collateral for incrementally borrowed ETH should be experimented with. We believe that the amount of reasonable collateral needed to slash an operator for misbehavior does not scale linearly with the amount of ETH they borrow from the deposit pool. For example, if they operate one validator, an example amount of collateral could be 4 ETH, but if they operate 8, there might only need to be 2 ETH per validator. The exact sublinear formula can be debated and explored at a later date.

We propose that depending on the total number of validators for a given node operator v, the total collateral requirement in ETH C(v) is given by: C(v) = C(1)*v^p

Using C(1)=4 ETH and p=⅔:

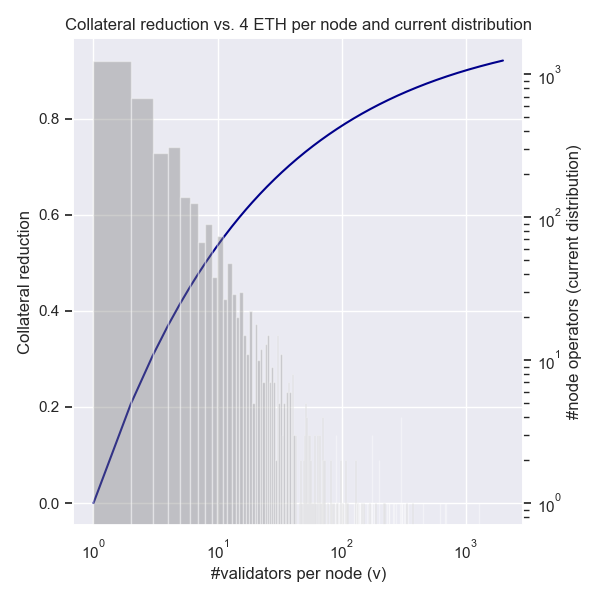

Currently, about 35% of nodes run one validator, so for them there would be no change in collateral if they run a minipool. However, for 20% of node operators who operate 8+ validators (in aggregate that is 80% of the validators), the reduction is 50% and potentially more:

The left axis/blue line shows 1 minus the ratio of proposed collateral needed per operator (operating v validators on the x-axis) divided by the current collateral needed when assuming 4ETH per validator. The right axis/gray bars show the current distribution, e.g. about 1200 operators running one validator. The conclusion is that compared to the world of vanilla LEB4, relatively less collateral is needed as the number of validators per node increases.

With slight updates to RPIP, we can efficiently lower the collateral requirement for larger node operators while reducing MEV-theft risk. This allows the protocol to support more demand at scale and ensure that the deposit pool remains empty, supporting maxETH’s main goal of maximizing rETH yields.

4. Optimize Deposit Queue Access for rETH APY

We expect that the Houston upgrade, accelerated by our delegation proposal, will lead to significant increases in deposit pool utilization. This raises the question of how to handle an empty deposit queue.

To address this, we propose prioritizing access to the queue based on the total RPL staked by a node operator (including delegated RPL). This approach ensures that those most committed to the protocol’s long-term health are given the first opportunity to serve the community. Additionally, it enhances protocol security by directing ETH towards operators who can provide the strongest security guarantees, as indicated by their slashable collateral.

To prevent centralizing forces in the deposit queue, we propose a mechanism where queue slots are reserved for new NOs. Additional protection avenues, such as limiting the number of slots per NO within a given timeframe, can be explored as part of further community discussion.

5. RPL Collateral for Node Operators

Given the newly proposed RPL delegation system, we also propose some tweaks to the current RPL collateral design. A fixed amount of 150 RPL will be required per validator, and this value will be static until the community or pDAO votes for a change.

Whilst the specific value is open to debate, our rationale for 150 RPL as the initial value is twofold:

- At current price levels, this adds approximately 1 ETH in collateral value per validator. This significantly increases collateralization for node operators running multiple validators and counter-balances the reduction in ETH collateral per incremental validator proposed in Bond Curves (RPIP-42). The result is maintained overall network security.

- Taking the current validator count, the theoretical required RPL stake of 150 equates to around 25% of circulating supply. This minimum threshold is a 50% reduction versus the current stake ratio of 50% coming from the current RPL staking requirement, but we believe our new RPL yield mechanism attracts staking beyond this new minimum of 150, and hence the drop in RPL staked under our new proposal in practice will likely be much less than 50%. Please click this here if you’d like to see some simulations we made around % RPL staked, RPL price, and more.

Static RPL values make it easier for both delegators and operators to track. The amount of RPL required per validator will not change regardless of how much a single node operator earns. If a node operator becomes undercollateralized, for example, when it does not have enough delegated RPL for the number of validators, there will not be a forced exit.

However, while a NO is undercollateralized, the full delegate_share is used to purchase RPL on the open market and stake it under the ownership of the pDAO. Once the node is sufficiently collateralized, the delegate_share reverts to the NO’s delegates. The pDAO continues to own the purchased RPL and benefit from its yield. A NO can not launch new validators while undercollateralized. One downside of an RPL delegation system is the elevated pressure on delegators to monitor their positions as they may temporarily be forfeiting their share to the pDAO.

The primary motivation for choosing a static value is to simplify life for NOs and delegators and alleviate the burden of constantly checking collateralization levels. An alternative approach would be to retain the mechanism where the required RPL is based on the value of ETH borrowed from the protocol. We are open to discussing this, as it has advantages and disadvantages, but believe the simpler approach is more suitable for this entire proposal.

A fixed amount of required RPL collateral minimizes the risk of prolonged periods where node operators lack sufficient delegations. This ensures a consistently optimal delegation market, allowing delegators to earn yields with the highest-performing node operators, thereby supporting maxETH’s goal of increasing rETH yields.

6. Introduce protocol-owned yield as part of the surplus share

We believe protocol commissions should, at present, only go to node operators and RPL stakers. However, in the future, one alternative value capture mechanism that is to be explored is the introduction of a protocol-owned staking pool where pDAO stakes the respective surplus share to earn yield on behalf of the protocol’s newly owned ETH assets. The subsequent yield is then distributed to rETH holders. This staking pool would be equivalent to the “surplus_share” recipient when referencing current proposals. The pDAO, guided by RPL voters, could select operators with less market share or more decentralized infrastructure and therefore counteract any potential centralizing forces that might result from crowding around the most performant NOs. This new scheme potentially strengthens rETH’s long-term APY, the primary goal of MaxETH, while simultaneously building up protocol-owned assets.

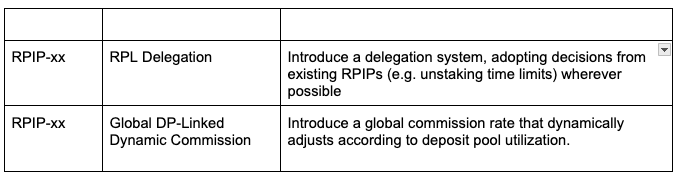

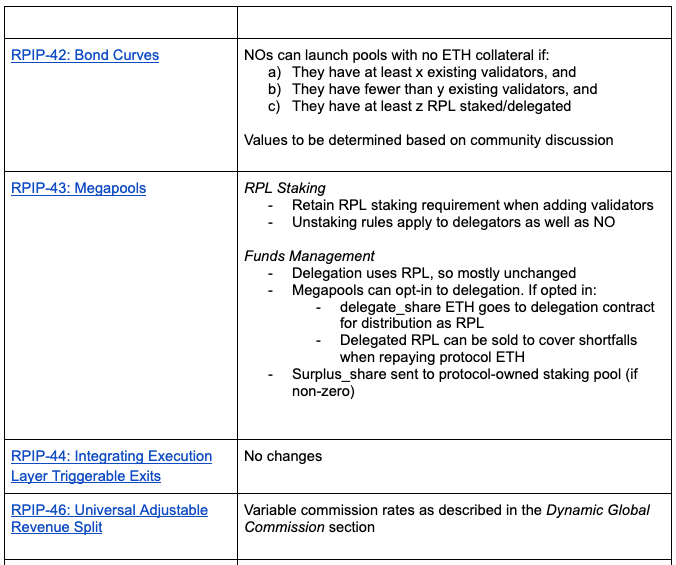

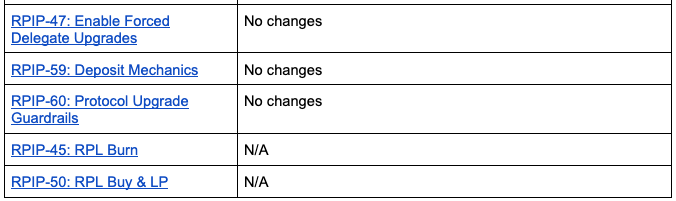

RPIPs - new and modified

Implementing this proposal would require two additional RPIPs, and modifications to multiple existing draft RPIPs. 1kx would provide the initial version of the new RPIPs and submit them to the community for discussion. We would also work with the authors of the existing proposals to integrate our changes in a way that minimizes the impact and allows us to continue along the previously accepted timelines.

Below is a high-level overview of the modifications we propose to the existing RPIPs:

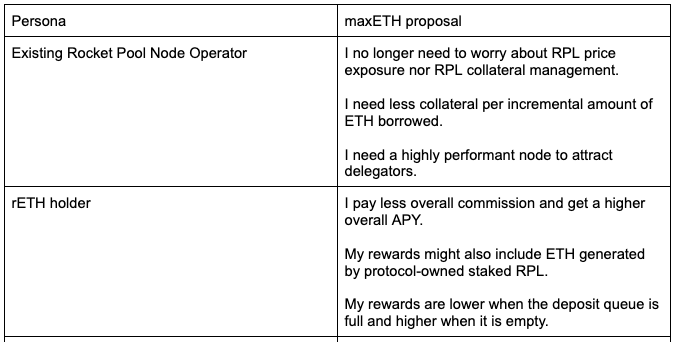

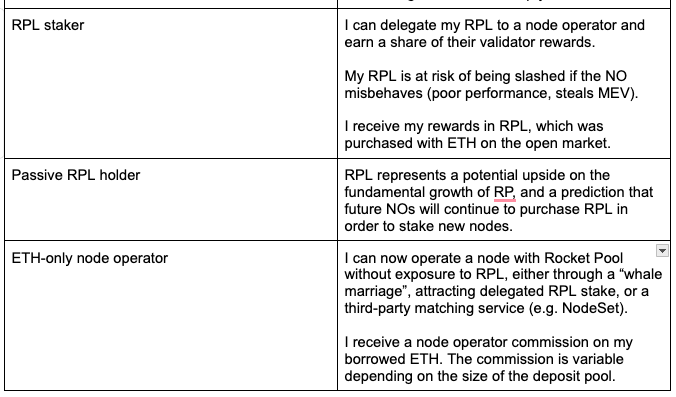

Personas

Concluding Thoughts

The maxETH initiative intends to increase rETH’s yield, making it the most desirable liquid staking product on the market. Meanwhile, we also aim to preserve the RPL collateral requirement, address the deposit queue buildup, and accelerate TVL growth, all of which are key to Rocket Pool’s future success. We believe that by modifying the existing rework to take full advantage of the Houston upgrade, one of the most exciting in the protocol’s history, we can create the most exciting liquid staking product on the market.

We appreciate your engagement and consideration of our post. We look forward to the community’s feedback and collaboration on refining and enhancing the current RPIPs. Your input is invaluable in shaping our collective future.

Disclaimers

Disclaimer: Rocket Pool is a 1kx portfolio investment.

Disclaimer: This article is for general information purposes only and should not be construed as or relied upon in any manner as investment, financial, legal, regulatory, tax, accounting, or similar advice. Under no circumstances should any material at the site be used or be construed as an offer soliciting the purchase or sale of any security, future, or other financial product or instrument. Views expressed in posts are those of the individual 1kx personnel quoted therein and are not the views of 1kx and are subject to change. The posts are not directed to any investors or potential investors, and do not constitute an offer to sell or a solicitation of an offer to buy any securities, and may not be used or relied upon in evaluating the merits of any investment. All information contained herein should be independently verified and confirmed. 1kx does not accept any liability for any loss or damage whatsoever caused in reliance upon such information. Certain information has been obtained from third-party sources. While taken from sources believed to be reliable, 1kx has not independently verified such information and makes no representations about the enduring accuracy or completeness of any information provided or its appropriateness for a given situation. 1kx may hold positions in certain projects or assets discussed in this article.