With the goal of protecting rETH’s value and increasing the RPL token’s utility within the Rocketpool ecosystem, this proposal aims to:

-

Introduce an RPL rerouting mechanism to compensate rETH holders and smoothing pool operators from intentional or unintentional node operator effectiveness underperformance. As of Aug 2023, the 15 largest “underperforming” NOs (based on # of minipools) were responsible for 33% of all CL penalties accrued by the protocol, and for 32% of all EL+CL missed rewards. (see “Top Offenders Analysis” section below)

-

Increase RPL utility within the protocol by auctioning the RPL rewards of underperforming node operators (or a portion their RPL bond if their collateralization level is below the 10%, or if their RPL rewards amount is insufficient). The ETH gathered from RPL auction is rerouted to compensate rETH holders and smoothing pool participants for the missed ETH rewards / penalties of underperforming node operators.

-

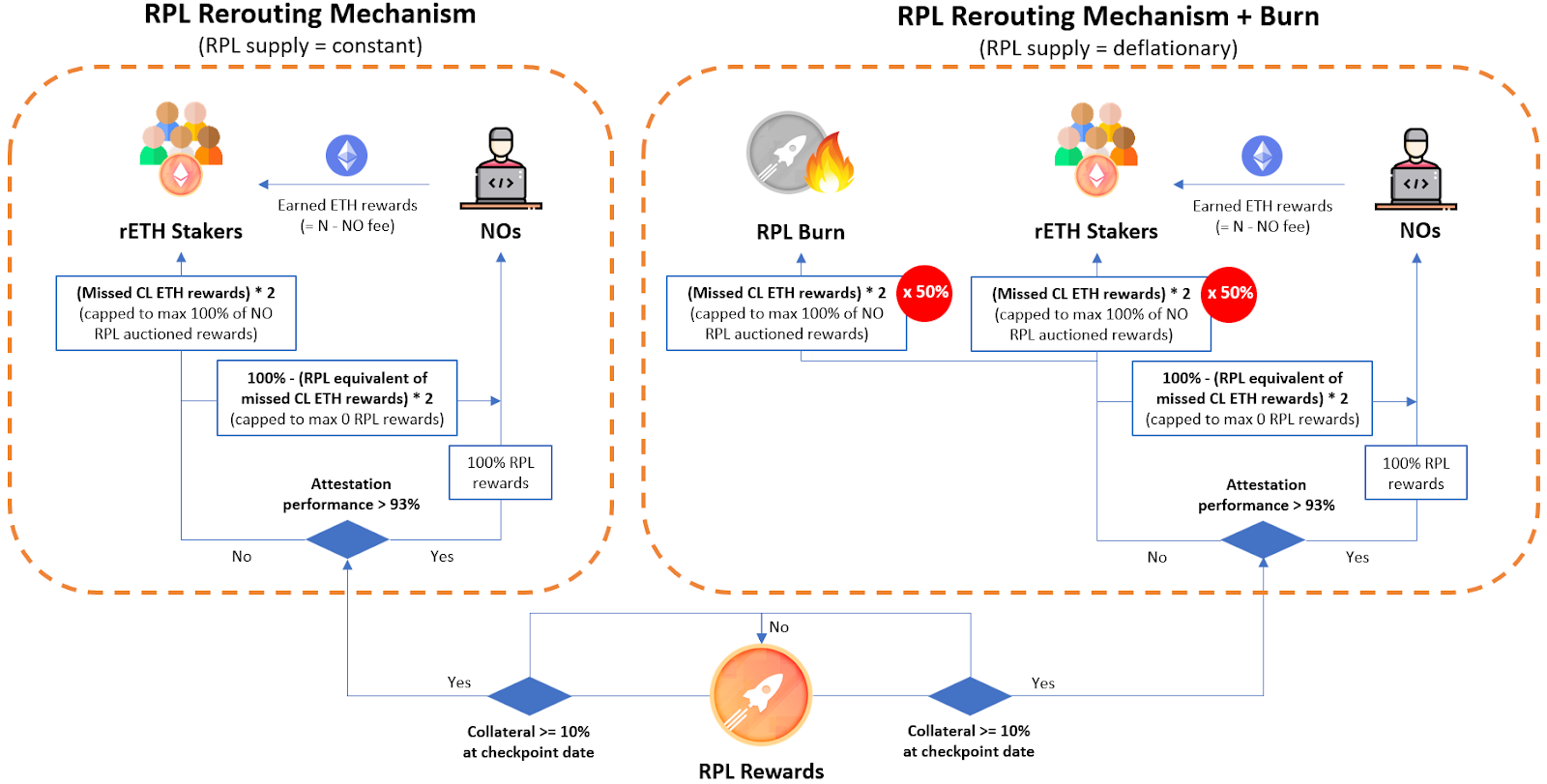

(TBD) Mirroring Ether’s burn mechanism introduced with EIP-1559, burn the equivalent amount of auctioned RPL to offset the RPL sell pressure caused by the RPL auctioning mechanism. Example:

- A node operator misses 0.25Ξ rewards in a period with an effectiveness below the defined underperformance threshold.

- 0.125Ξ worth of the node operator’s rewards (or RPL bond if rewards are insufficient/unavailable) is rerouted, auctioned off, and sent to the rETH and smoothing pool porportionately.

- 0.125Ξ worth of the node operator’s rewards (or RPL bond if rewards are insufficient/unavailable) is burned, offsetting the structural sell pressure created by the RPL rerouting mechanism.

→ Details and visuals of RPL rerouting are presented in detail in the “Low Node Operator Performance Disincentives Proposal” section below.

A backstop mechanism for RPL rerouting needs to be discussed and implemented in case of protocol-wide events (e.g. a client or protocol bug) which cannot be attributable to individual node operator performance.

Background

As of August 2023, Rocketpool was the worst-performing staking pool in terms of effectiveness among the top 10 staking entities, both in all time and trailing 30D effectiveness. As of Dec 2023, the protocol’s effectiveness performance has dropped even further, standing at 93.79% T30D effectiveness rating as per rated.network vs 95.5% in Aug 2023.

When we break down this effectiveness underperformance level to a node operator level, we saw that the top 15 underperforming Rocketpool node operators, which made-up 4.7% of the Rocketpool network, represented 33% of all Consensus Layer (“CL”) penalties accrued, and 32% of all (ETH) missed rewards in the last 30 days as of Aug 2023. (see details in the “Top Offender Analysis” section below)

Therefore, this proposal aims to achieve the following goals, guided by a balance between pragmatism, which a quality required to succeed in any competitive market environment, and idealism, which should continue to drive the Rocketpool community forward. It:

1. APR Improvements (for both liquid stakers and node operators) through a partial rerouting of RPL rewards of bad performance outliers towards protecting rETH and the smoothing pool, while introducing deflationary economics for the RPL token, in line with Ethereum’s EIP-1559 burn principle.

2. Stronger but “flexible-enough” performance standards which avoid centralization vectors at all costs (i.e. avoiding effectiveness performance levels which would fit mostly to professional stakers with high-end equipment).

While all the data presented in this proposal is of Aug 2023, I managed to obtain access to the rated.network API for Rocketpool-related purposes, in order to update all metrics to the latest status, expand timeframes as required, analyse the full long tail of node operators in detail, and set-up reporting required to track metrics/KPIs relevant to this proposal.

Importance of high effectiveness for the Rocketpool protocol

Performing at a low effectiveness rate against other protocols de facto means that the Rocketpool protocol will probabilistically deliver a lower APR for all of its ETH (and rETH)-denominated capital. More specifically, in an ever-growing competitive market for liquid staking protocols, an uncompetitive APR:

- … dilutes rETH’s attractiveness as an LST alternative vs other protocols (APR-wise).

- … hinders Rocketpool’s decentralisation goals by making it less attractive for “small” node operators to join the protocol (potentially even the smoothing pool in particular), since these will typically face more unfavourable set-up and operational costs per unit of income generated (compared to whales and mid-size stakers). As an example of this:

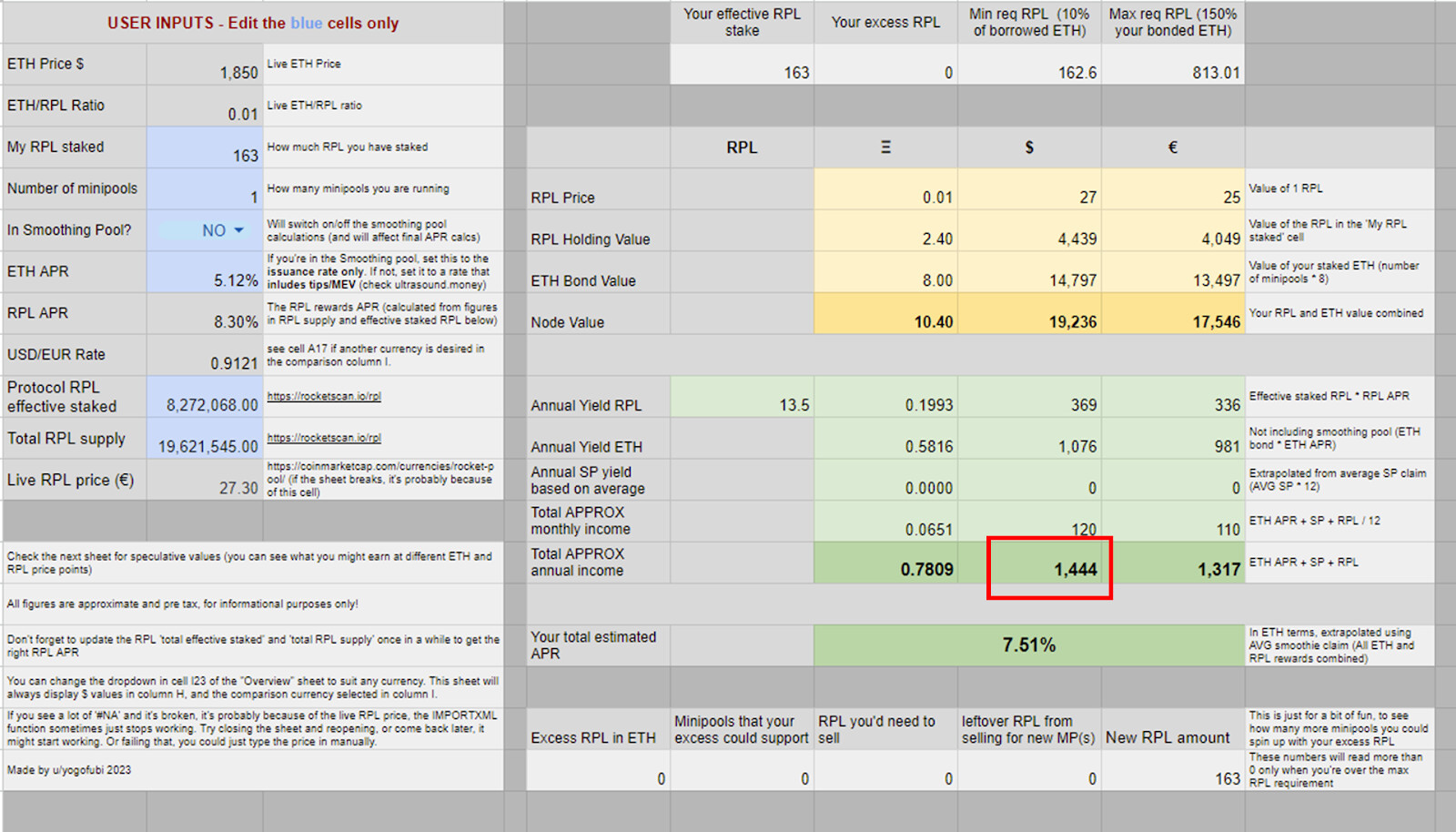

- 1 self-operated LEB8 carries a fixed hardware set-up cost between $500-$1500, while at current prices and returns (Snapshot: 12/08/2023) an LEB8 would yield $1,444 after 1 year of operation incl. RPL rewards. The 1yr Cost/Income ratio in this case is about 1:1. See Appendix 1 for details on staking returns.

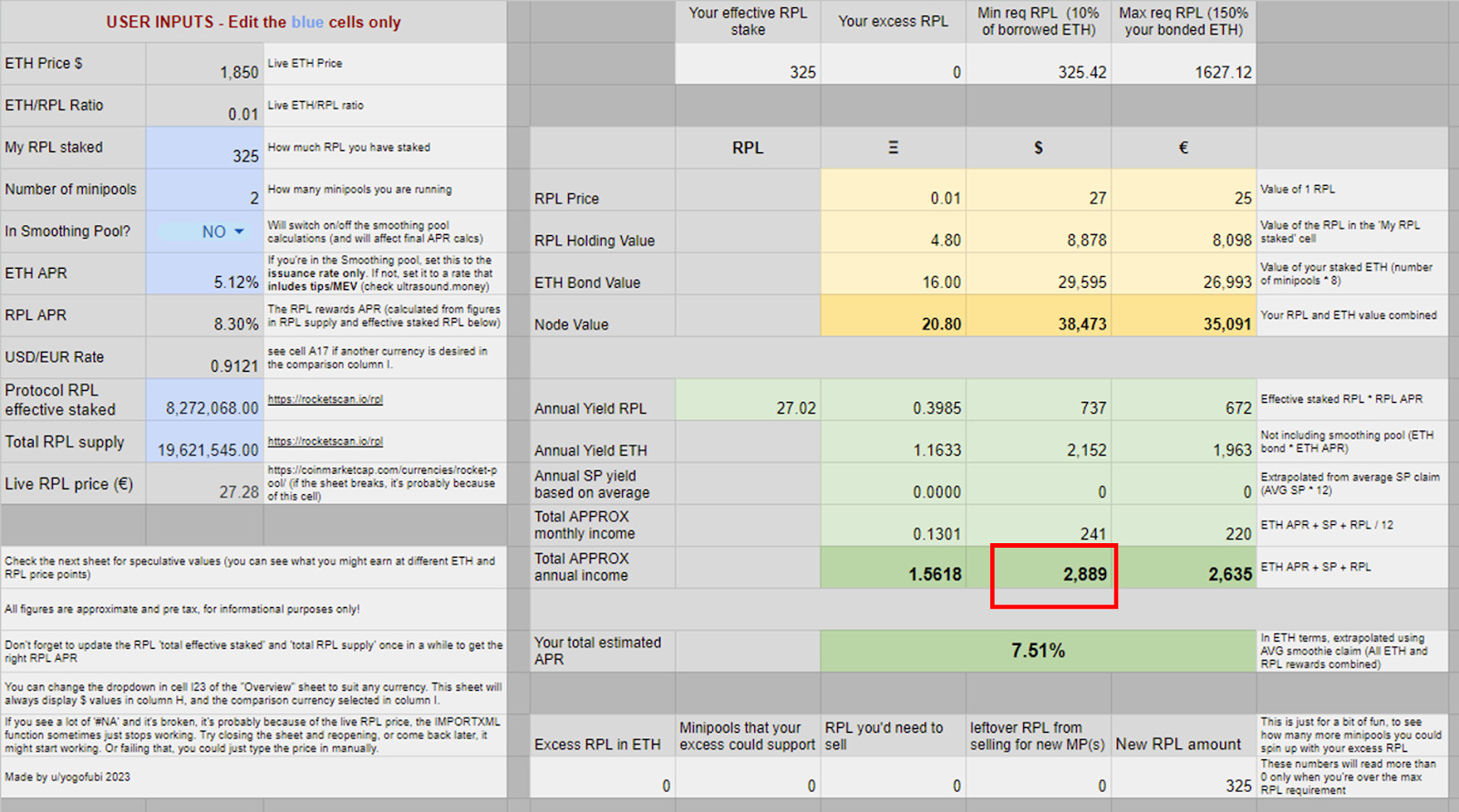

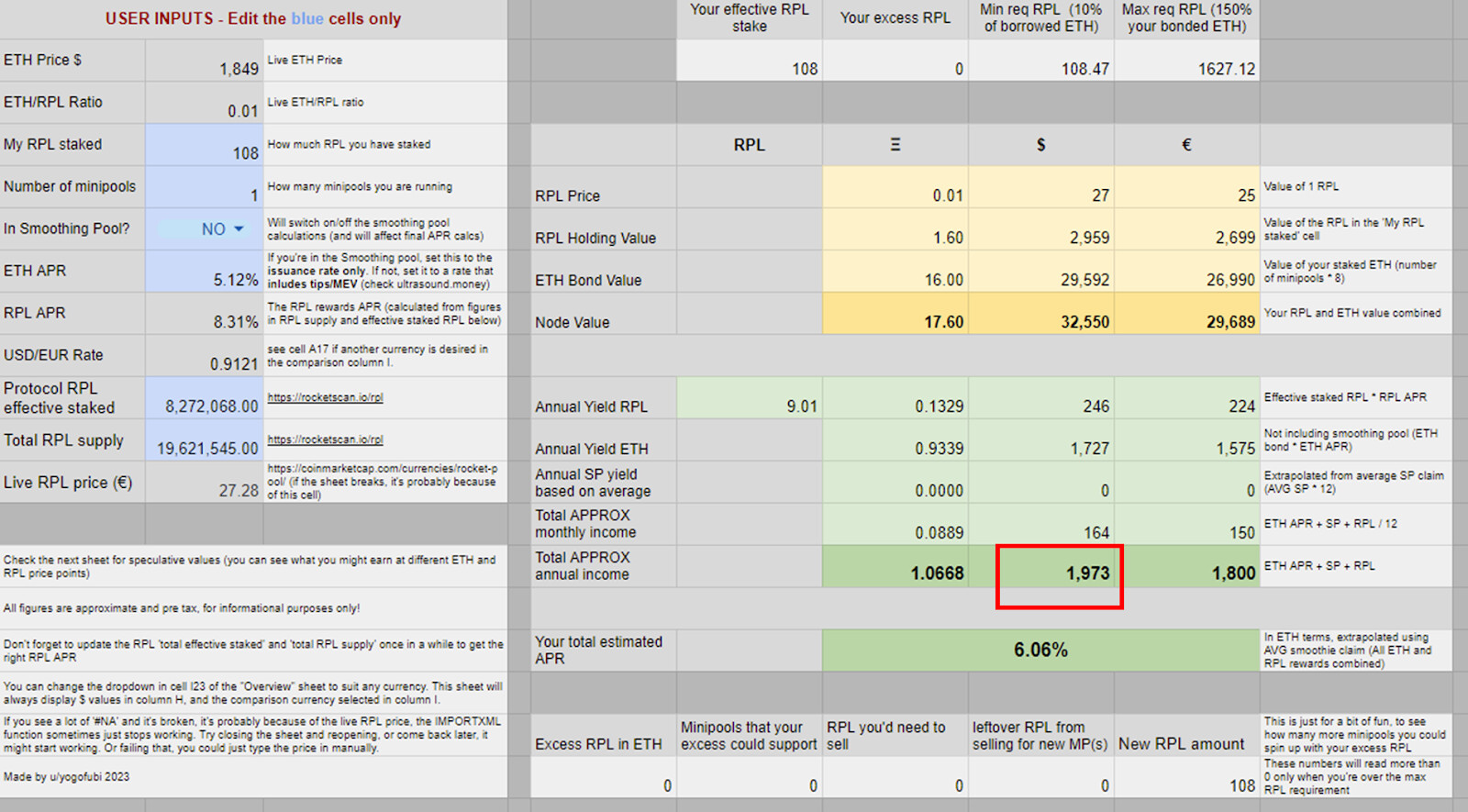

- 1 self-operated 16 ETH minipool, or 2 self-operated LEB8s, will yield $1.973 or $2,889 respectively, for the same cost. The 1yr Cost/Income ratio here is about 1:1.5-2.

- 1 professional staking set-up managing 300-500 LEB8s can generate between $400k - $700k annually. The 1yr Cost/Income ratio in this case is about 1:4-10 (rough estimation based on feedback gathered from the Rocketpool community on professional staking set-up costs).

- … ultimately hinders Rocketpool’s growth and attractiveness against other growth-optimised competitors.

Effectiveness Performance Break Down

Large Operators vs the Rest - an 80/20 Analysis

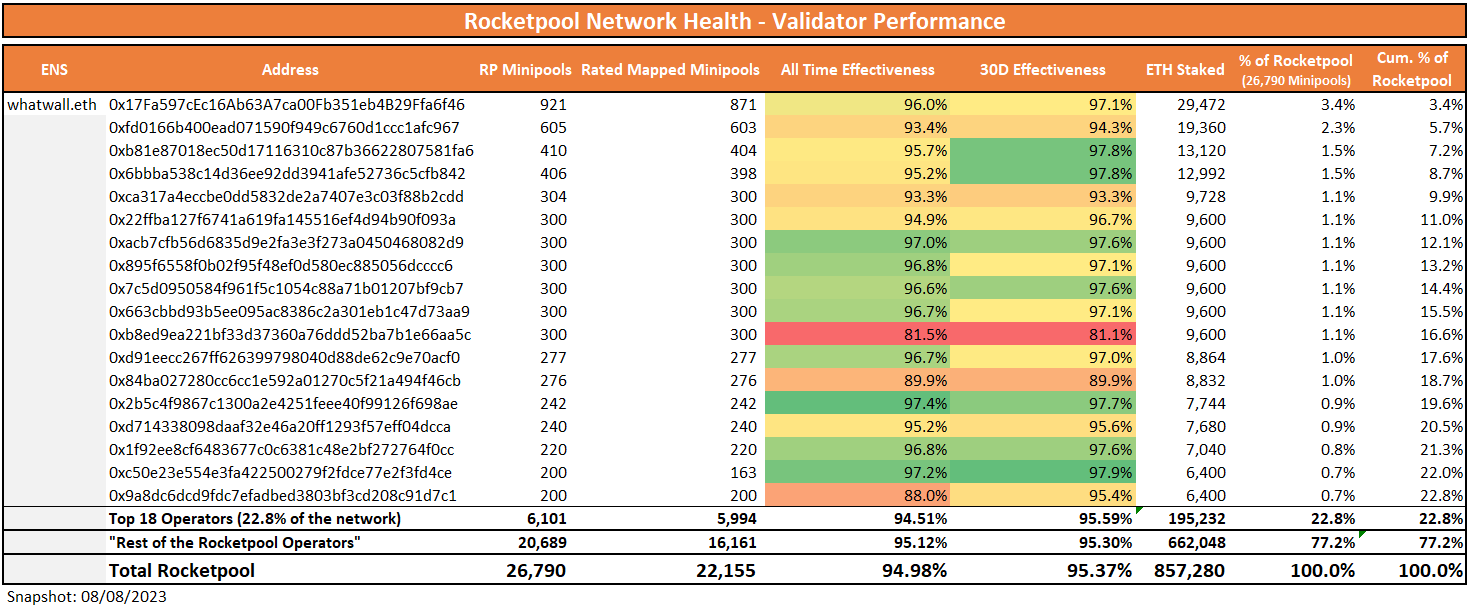

As seen in the table below, the protocol’s current low effectiveness as of Aug 2023 does not seem to be a “big operator” or “small operator” problem. The top 18 Rocketpool node operators (“NOs”) (based on # of minipools), who represent 22.8% of the Rocketpool network, and who all have >= 200 minipools in operation per NO, have a lower all time effectiveness vs the overall Rockepool effectiveness (and lower than the rest of “smaller Rocketpool operators”).

On a 30D horizon, the effectiveness of these top 18 operators is in line with the total Rocketpool network’s average, and in line with the effectiveness of the rest of smaller Rocketpool operators. See discussion around this analysis in the Rocketpool # | research channel.

While this analysis should be broken down in smaller n sample cohorts as a second step (which would help us understand different personas and profiles among Rocketpool’s 3k node operator set), for the purpose of this proposal, the size-based effectiveness performance analysis will be left at this level.

Top Offender Analysis - The few which drive the most

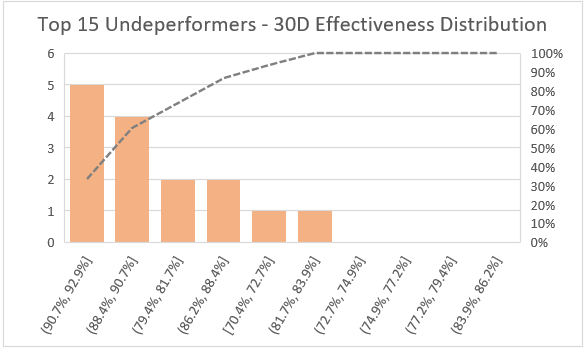

If we look at it from the angle of the “worst and largest underperforming nodes”, out of the top 75 node operators (based on # of minipools), 20% perform at effectiveness levels below 93%. While we should analyse the full set of Rocketpool node operators to identify the optimal effectiveness % level upon which a minimum adequate performance threshold should be set, for the purpose of this analysis I set the threshold at 93% since that covers 20% of the the 75 top underperformers cohort (striving to follow a Pareto principle). The distribution of these 15 “underperformers’‘’ effectiveness is portrayed in the chart below.

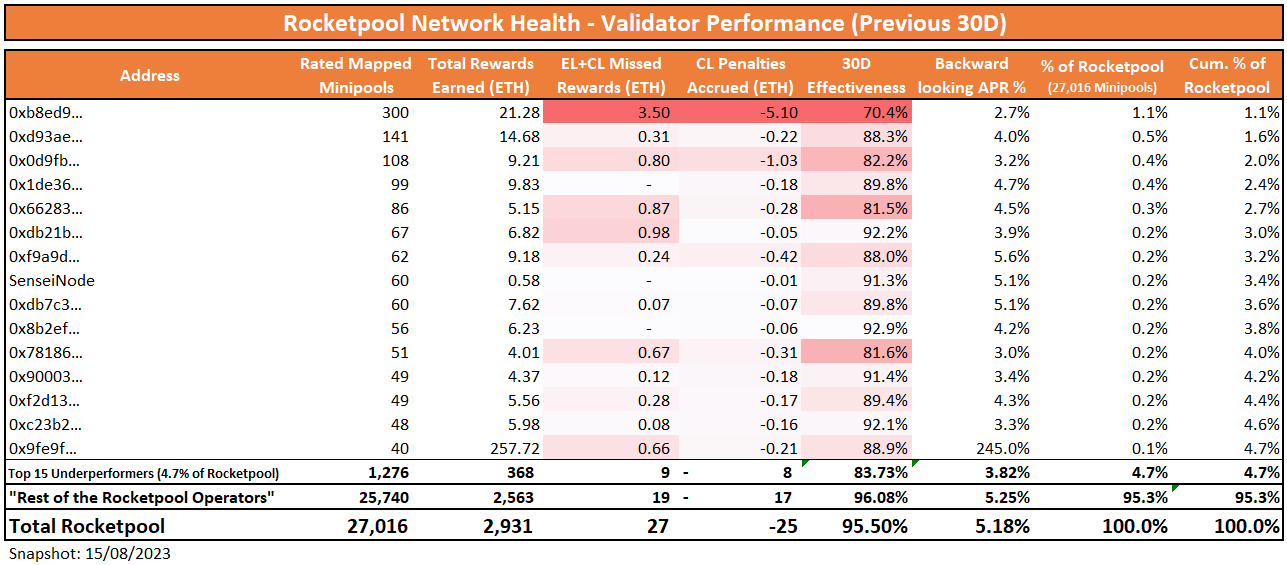

As seen in the table below, as of Aug 2023 these 15 underperformers represent 4.7% of the Rocketpool network (based on # of minipools), but are responsible for 33% of all CL penalties accrued in the last 30 days (as of Aug 2023), and for 32% of all EL+CL missed rewards (source: rated.network).

These underperformers costed the Rocketpool network 0.07% APR if we extrapolate their performance to 1yr:

(25Ξ CL Penalties + 27Ξ Missed EL+CL Rewards) *12 / (27,016 validators * 32Ξ) = 0.07% lost APR

Performance Analysis Conclusions

As presented in the analyses above, the data 1) initially confirms that low effectiveness is an issue which is neither specific to the top/largest 20% Rocketpool network, nor to the remaining 80% made out of smaller NOs. At the same time, 2) we see that >30% of all lost protocol income is driven by a small percentage (4.7%) of the network. Finally, it seems that 3) income loss occurs in a similar magnitude both for CL penalties, as well as for EL+CL missed rewards (this observation should also be confirmed for the entire set of Rocketpool NOs, since it is relevant for the low performance disincentives logic proposed up next).

These 3 findings enable a positive and realistic outlook for the idea of applying disincentives on the “underperformer” cohort, which is the goal of this proposal. This statement is based on the fact that, if we were to apply disincentives towards underperformers:

- Disincentives would be applied in an evenly distributed way across the NO set, without affecting the top 20% or bottom 80% NO cohorts in particular (finding 1).

- Disincentives would not have to affect a significant portion of the Rocketpool NO set in order to drive a material performance improvement (finding 2). It is important, however, that disincentive criteria follows a minimum acceptable performance level defined by an absolute reasonable effectiveness % level, and not by a “bottom X%” logic, since the latter could eventually spiral up to performance values that drive centralization towards professional operators.

- Disincentives could be applied leveraging the current smoothing pool attestation effectiveness logic since, it seems that CL offline penalties (e.g. -25 ETH, which are measurable through attestation effectiveness) are 1:1 correlated with the (opposite sign) magnitude of missed EL+CL rewards (e.g. 27 ETH) (finding 3).

In particular, the disincentive proposal outlined in this paper presents the idea of RPL staking reward reductions (or reduction of a NO’s RPL bond), which should in turn be channelled towards rETH APR protection by leveraging a similar mechanism as the existing RPL auction (see the “Low Node OperatorPerformance Disincentives Proposal” section below for further details on this).

By doing so, we would effectively:

- Surgically add disincentives for NOs who intentionally or unintentionally lower rETH’s APR.

- Improve RPL’s current binary rewards logic (collateral ratio >10% of borrowed ETH = Y/N).

- Make rETH whole for extreme cases of NOs underperformance, while giving RPL a new protocol function.

- Add deflationary forces to RPL’s tokenomics.

Low Node Operator Performance Disincentives Proposal

This proposal strives for RPL rewards, which are currently given to NOs based on a binary criteria (collateral ratio >10% of borrowed ETH), to go through a second evaluation layer which looks at NO performance. In particular, this second layer should check whether NO’s attestation effectiveness (an existing KPI/logic used for smoothing pool reward distribution) stands above a defined minimum attestation performance level defined for the protocol (e.g. >= 93%, in the “Top Offender Analysis” example shared above). If not, the RPL equivalent of the CL ETH offline penalties, times 2 (see finding 3 above on why the x2 multiplier could be applied to also account for missed EL rewards), would be auctioned for ETH using the existing RPL auction mechanism, and channelled to the rETH rewards pool and to the smoothing pool.

Additionally, in order to mitigate the potential “constant” RPL sell pressure which this mechanism would cause, an additional variant would be to channel 50% of the missed ETH rewards towards making rETH holders whole, while burning the remaining 50%. This is inspired by Ethereum’s EIP 1559 principle to accrue value towards the burned token itself. This would, in the mid- to long-term, offset entirely the sell pressure created by auctioning RPL of underperforming NOs for ETH.

Finally, in cases where the NO’s rewards of a particular round are not enough to offset the “damage repair” required for that period due to underperformance, or in case the NO is under 10% collateralization ratio and would not receive rewards for that specific period, then a portion their current RPL bond should be utilized to make rETH and node operators whole. (this last point is not covered in the flow charts above, which assumes that RPL rewards of a NO are always enough to cover the missed rewards/penalties)

Appendix 1: Staking Return Detailed Calculations

Source: Staking Calculator and P&L - ArtDemocrat (built on top of @yugofobi’s staking calculator - full credits on the “APR Calc.” and “Speculative” sheets)

1-Year return calculation for 1 LEB8, collateralized at 10%:

1-Year return calculation for 1 16 ETH Minipool, collateralized at 10%:

1-Year return calculation for 2 LEB8, collateralized at 10%: